IoT revenue and connections continue rapid, but not explosive, growth

Operators’ enterprise reporting is poor and reporting on IoT is even worse. We are aware of only four operators (Telstra, Telefónica, Verizon and Vodafone) that regularly report IoT revenue, and only 11 that report connection numbers. For a segment that is supposedly key to future growth, operators are remarkably shy about providing progress updates.

The operators that do provide information are, by definition, atypical. That they are providing data at all probably skews the sample. We can, however, still glean some useful insights by exploring the data that is available.

IoT revenue growth is fast, but may not be fast enough

The key metrics for the IoT business are positive for almost all operators, with rapid, if not explosive, growth, but IoT remains a relatively small part of a mobile operator’s business. If growth were to slow, it could raise some difficult questions, especially for less committed operators.

The main points from the financial results are the following.

- IoT revenue grew quickly for all operators. Operator IoT revenue grew between 7.9% (Telstra) and 30.4% (Telefónica) during the calendar year 2017, compared to 2016. Verizon’s figure was higher (we estimate that it grew by 70%) but is not comparable as much of this growth was due to large acquisitions. The average organic growth rate (15%) is comparable to that for other IoT companies or divisions, such as Intel’s IoT Group (which grew at 20.1%).

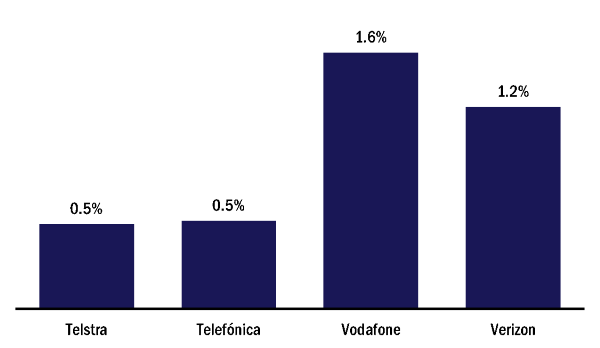

- IoT is still only a small part of operators’ business, despite the fast growth. For each of the four sample operators that provide data, IoT constitutes less than 2% of their total revenue (Figure 1). Even at an annual growth rate of 15%, it would take until 2026 for an operator to grow IoT from providing 1.6% of the total revenue to over 5% (assuming a flat top line). All of this has implications for IoT divisions within operators; IoT is likely to be a long, hard struggle, and teams will have to fight to gain resources and attention from other parts of the company. It also suggests that more radical approaches (such as that Verizon has taken through acquisition) may be necessary to grow faster.

- IoT is already a USD1 billion business for some operators. In absolute terms, especially for the larger operators, IoT already generates significant revenue. IoT is worth over USD1 billion a year for Verizon, probably more for AT&T (it does not split out IoT revenue) and EUR720 million (USD890 million) for Vodafone. If IoT were a standalone business, it would be considered large; it is only small in comparison to the core business.

- IoT may help to defend existing revenue. IoT may have a value beyond the direct revenue opportunities. As more organisations require IoT solutions, they may want to buy all connectivity, traditional mobile as well as IoT, from a single connectivity provider. A strong IoT offering may be needed for an operator to defend its broader enterprise communications business. We have heard of operators using IoT as a beachhead from which to bid for larger enterprise contracts.

Figure 1: IoT revenue as a share of the total revenue, 2017

Source: Analysys Mason, 2018

Connections are also growing extremely quickly, even from a high base

The number of IoT connections is also showing fast growth. The key points to note here are the following.

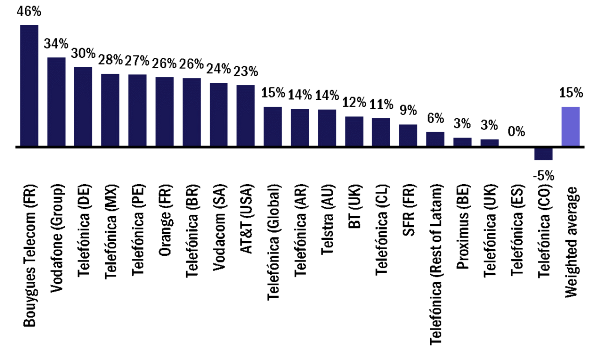

- Scale may be helping some of the larger operators to grow more quickly. As we can see in Figure 2, almost all operators are seeing rapid growth in the number of connections, even from a relatively high base. For example, Vodafone grew its connection numbers by 34% in a year, taking it from just under 50 million at the end of 2016 to around 65 million by the end of 2017. Scale may even be helping the operators with a large base to grow faster – operators with a large base will have a big base of reference customers, have (in most cases) mature systems and processes, and may be willing to offer lower prices as any fixed costs will be spread across a larger base. Clearly, this scale factor is not universal – the fastest growing operator of all was Bouygues Telecom in France, which had fewer IoT connections than local rivals Orange and SFR.

Figure 2: Growth in the reported number of IoT connections, 2016–2017

Source: Analysys Mason, 2018

- Connection numbers can go down as well as up. As the results from Telefónica Colombia show, it is not a given that the number of IoT connections will increase for a telecoms operator. The loss of a major contract or the cancellation of a large-scale pilot can lead to a fall in the number of connections. While over a year, the connection numbers tend to grow, we have also seen other operators face quarter-on-quarter declines in the number of connections (for example BT’s connection numbers for 3Q 2017 were slightly down on those from 2Q 2017).

- The average revenue per connection (ARPC) is falling for most operators, but not for Telefónica. For Telstra and Vodafone, connections are growing more quickly than revenue. For Telefónica though, the reverse is true. This suggests that either Telefónica’s ARPC is growing, or it is having success in selling more than just connectivity (or both). Whatever the reason, it is an encouraging result for Telefónica. On average, revenue per connection is falling by between 5–10% per year. If we assume that average contract lengths are two years, this means that (all else being equal), contracts are being renegotiated at around a 10–20% discount – not dissimilar to enterprise mobile contracts. This still suggests that there is strong price competition and that operators have been unsuccessful in moving away from pure price competition for IoT contracts.

We will be updating our IoT price and connections tracker each quarter and may provide further commentary on the data.

Downloads

Article (PDF)Authors