Operators must adapt their strategies to capture growing high-bandwidth IoT connectivity revenue

"IoT connectivity revenue is concentrated in a small number of high-bandwidth applications."

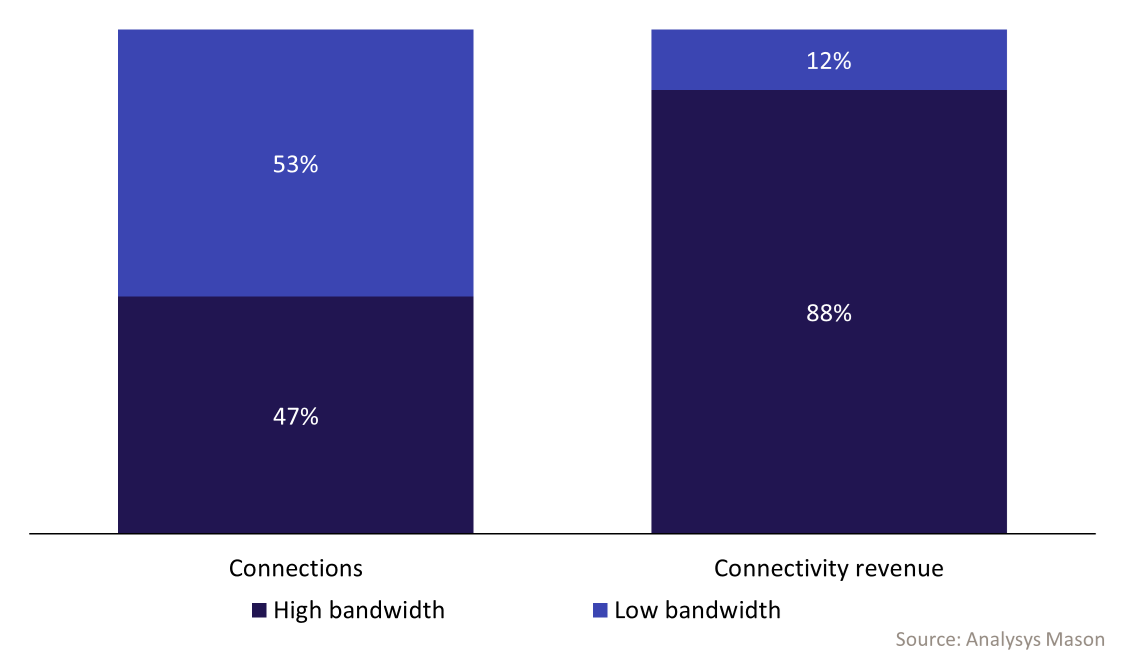

![]()

IoT connectivity revenue is poised for substantial growth over the next decade. Analysys Mason forecasts that worldwide revenue will almost double between 2025 and 2034, from almost USD17 billion to over USD30 billion. Over the same period, the total number of IoT connections will increase from more than 4 billion to over 8 billion.

However, revenue growth will not be distributed equally within the IoT connectivity market. This largely comes down to a divide between high-value, high-bandwidth applications and low-value, low-bandwidth applications. Differences in data consumption drive this segmentation, which, in turn, affects the average revenue per connection (ARPC).

While the IoT market’s ARPC experienced long-term decline, this is expected to moderate as high-bandwidth applications scale. ARPC fell at a CAGR of 7% between 2020 and 2024, but this decline is forecast to slow to 2% between 2025 and 2030 (worldwide, excluding China).1

High-bandwidth applications already account for a disproportionate share of connectivity revenue compared to that of high-bandwidth connections (Figure 1). This pattern is expected to become more pronounced over the next decade. Operators will have to adapt their strategies to generate revenue. Diversifying and serving the long tail in high-bandwidth applications will offer the best opportunities to do so.

Figure 1: High-bandwidth share of wireless IoT connections and connectivity revenue, world, excluding China, 2025

The utilities and automotive sectors dominate the low-bandwidth and high-bandwidth IoT segments, respectively

Connections in each IoT market segment are concentrated around a single dominant vertical: automotive takes the lead for high-bandwidth applications, and utilities dominates the low-bandwidth segment.

Both segments feature large, regional deployment contracts that are typically awarded to a small number of suppliers. This contract structure favours large, established connectivity providers with the scale and operational capacity to support significant connection volumes.

Together, these verticals accounted for almost half of worldwide IoT connections in 2025 (again, excluding China).

Automotive is the largest IoT vertical by connectivity revenue and connections

The automotive sector generated almost half of worldwide IoT connectivity revenue in 2025 from 400 million connections (excluding China). Factors that support growth in connections include near-universal adoption of embedded SIMs in new vehicles sold in high-income regions and strong year-on-year growth in car sales in middle- and low-income markets.

Growing data usage per vehicle is also driving automotive revenue. Automakers are increasingly deploying data-intensive applications, including video telematics and advanced driver assistance systems. The rising adoption of electric vehicles (EVs) amplifies this trend: EVs typically generate several gigabytes of data per month, compared with 50MB to 1GB for internal combustion engine vehicles.

Utilities dominates the low-bandwidth segment

Utilities accounted for 240 million IoT connections in 2025 and USD350 million in connectivity revenue (excluding China). Utility connections usually transmit small, periodic data packets, such as meter readings or fault alerts.

However, utilities deployments provide long-term revenue through large-scale smart-meter contracts that can span ten years or more. Many metering contracts have already been tendered in European markets, but opportunities remain in countries in other regions. Examples include Telefónica’s deployment of 4.4 million NB-IoT water meters in Brazil from 2025 and Airtel’s deployment of 20 million electricity meters in India from 2024.

Smaller players can generate revenue by serving the long tail of IoT applications

Smaller connectivity providers will struggle to secure large automotive and utilities contracts. Instead, they should focus on the fragmented long tail of IoT applications.

Several smaller high-bandwidth applications generate meaningful revenue, despite relatively limited connection volumes. For example, in the healthcare vertical, customers are willing to pay a premium for connectivity because reliability and security are critical. Remote patient monitoring offers a particularly attractive option for operators: it requires continuous, secure connectivity and delivers a higher ARPC than many other IoT use cases.

Security applications, including connected cameras, are also emerging as an important revenue opportunity in the high-bandwidth segment. Cellular connectivity provides a flexible and often more cost-effective alternative to wired solutions, supporting adoption across commercial and residential markets.

Opportunities in the low-bandwidth segment can provide scale. For example, tracking accounted for more than a tenth of global IoT connections in 2025 (excluding China). Adoption is rising due to improvements in device form factors, including iSIM smart labels, and network technologies. For example, use of LTE Cat-1-bis to track deployments is growing. It offers benefits such as roaming on LTE networks and module pricing comparable to that for LTE-M.

Tracking deployments typically involve large volumes of devices that transmit infrequent location updates or environmental readings, providing a secure base of IoT revenue.

A greater share of high-bandwidth applications will help operators secure sustained IoT revenue growth

The divide between high- and low-bandwidth applications will increasingly define the IoT market. Automotive and utilities will continue to dominate these respective markets. However, future revenue growth will be concentrated in the long tail of other high-bandwidth IoT applications.

Operators should therefore diversify their presence in the high-bandwidth segment, such as in healthcare or security applications. A greater number of high-bandwidth applications will enable them to support revenue growth while preserving their scale in low-bandwidth segments.

Analysys Mason brings extensive experience in IoT, gained through research and customer projects. Our expertise can help stakeholders capture revenue growth opportunities in IoT. For further information, get in touch with Ibraheem Kasujee, the head of our IoT Services programme.

1 China accounts for a third of worldwide IoT connectivity revenue and two thirds of IoT connections. It will be excluded from market totals in this article because it is a large and unique market, which distorts global trends. For more information, see Analysys Mason’s China: wireless IoT market trends and forecasts 2025–2034.

Download

Article (PDF)Author

Mary Saunders

AnalystRelated items

Article

MWC26: IoT and private networks were less visible than in the past, but steady progress continues

Forecast report

UK: wireless IoT market trends and forecasts 2025–2034

Forecast report

Italy: wireless IoT market trends and forecasts 2025–2034