Strategic ecosystem alignment will fuel growth in the satellite-enabled connected car market

"Connected cars represent a major growth driver for satellite operators, but capturing the opportunity will require fundamental shifts in integration, monetisation and terminal strategy."

Satellite-enabled connected cars present a huge growth opportunity for the space industry, but a commercial breakthrough seems distant in the current ecosystem. The main constraint is not satellite availability or lack of consumer interest but a structural misalignment between vehicle design, integration of hybrid terrestrial and non-terrestrial networks (NTNs) and the business models in place for monetising this connectivity. To make satellite connectivity integral to future mobility, satellite operators and original equipment manufacturers (OEMs) first need to embed satellite connectivity as a basic service. This process should focus on safety through emergency and location sharing in the software-defined vehicle (SDV) stack before expanding to other services.

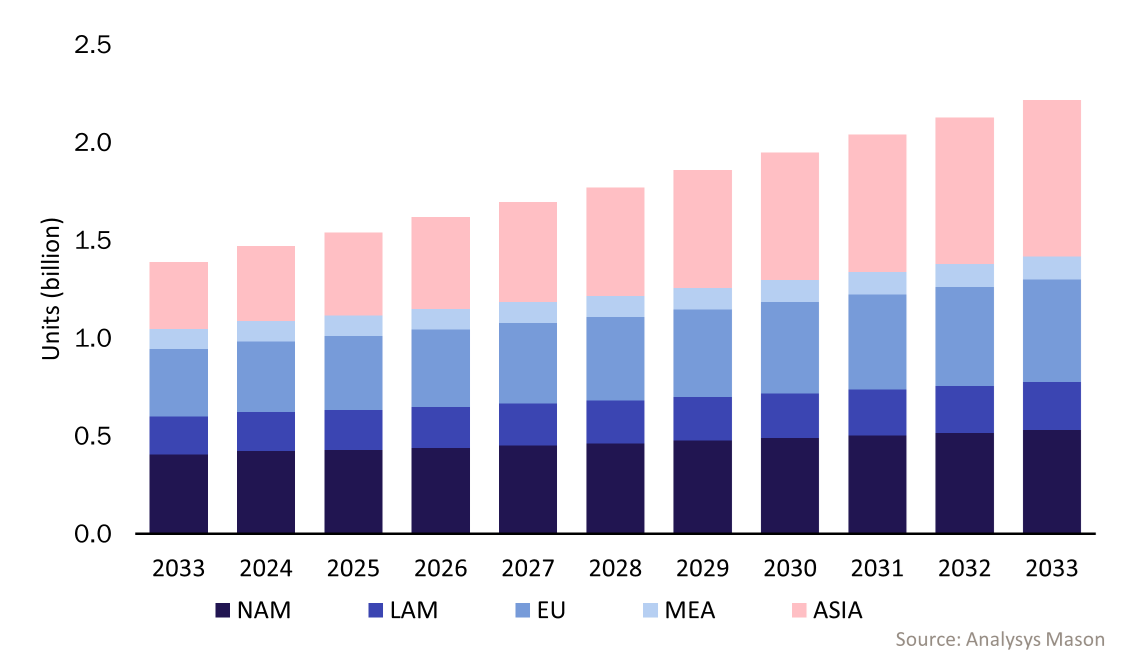

The satellite-enabled connected car market offers significant potential for growth. Analysys Mason’s research into trends and forecasts for satellite mobility addressable markets projects that satellite-enabled automotive connectivity will generate USD74 billion in cumulative retail revenue over the next 10 years, positioning connected cars as one of the most important emerging verticals for the satellite industry (Figure 1). This is not just a short-term opportunity; it represents a long-term growth driver spanning safety services, coverage extension, telematics and fleet applications, as well as data-intensive use cases like over-the-air updates and infotainment systems.

Figure 1: Satellite connected cars addressable market 2023–2033

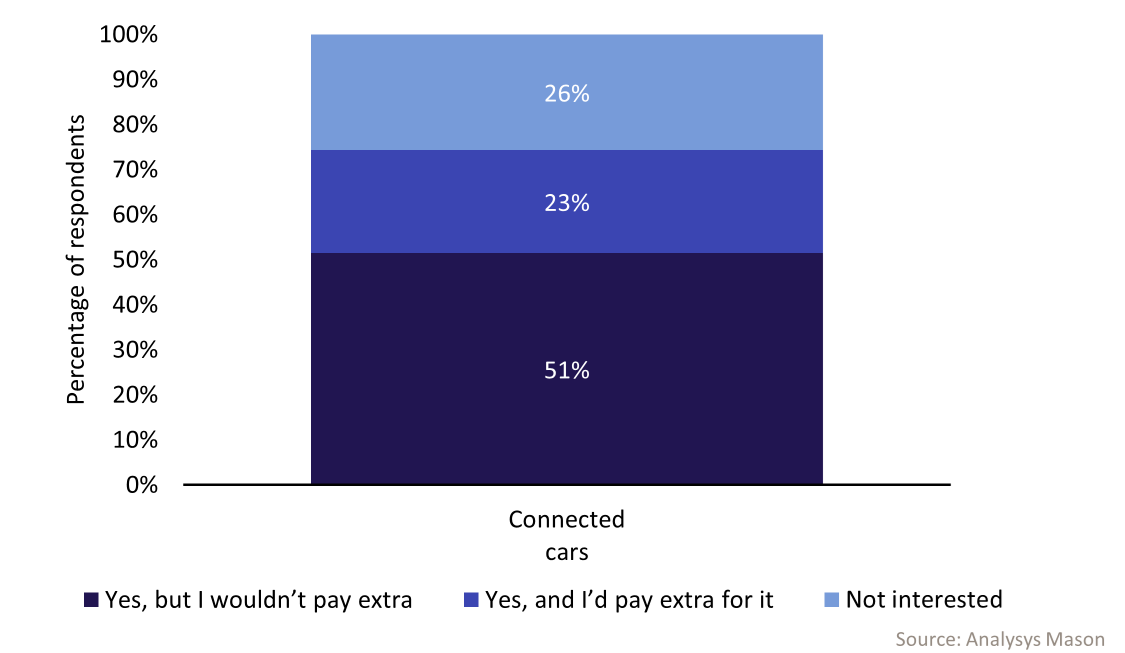

Consumer sentiment reinforces the feasibility of this opportunity, particularly when it comes to resilience and safety. The results of Analysys Mason’s consumer survey on satellite-enabled emergency and location sharing in cars show strong latent demand for these services. 74% of respondents expressed interest in access to satellite connectivity for emergency services, indicating that ‘always-on’ coverage plays an important role in safety use cases and gives consumers peace of mind. However, willingness to pay is lower. Only 23% of respondents are willing to pay for such services, though this percentage varies by age, income and location, with younger, higher-income and urban segments more likely to select this option (Figure 2).

Figure 2: Consumer interest in satellite-enabled basic emergency and location-sharing services in cars, total panel, 2025

Interest in satellite-enabled emergency and location-sharing services significantly exceeds stated readiness to pay, which indicates a price-sensitive market where consumers view basic connectivity as a standard feature. The demographics that showed greater willingness to pay provide a starting point for monetising advanced features in premium vehicle trims.

Together, these dynamics point to a clear conclusion: there is a sizeable addressable market, but to capture value, operators will need to align pricing, positioning and integration strategies with the areas that reveal the strongest consumer interest.

Rebalancing economics and integrating terrestrial and non-terrestrial networks at scale

Unlocking the potential of connected cars will rely on improving the underlying economics while delivering seamless integration between terrestrial and non-terrestrial networks. These two actions are interdependent: service quality suffers in the absence of efficient hybrid integration, and large-scale deployment becomes commercially fragile without sustainable monetisation.

From an economic perspective, satellite connectivity in the automotive industry cannot rely solely on price-per-gigabyte models. Use cases vary widely in data intensity, latency sensitivity and criticality. Narrowband safety signals, periodic diagnostics and software updates generate very different network loads and value outcomes compared to high-bandwidth infotainment. As a result, pricing models must evolve into service-aware structures that reflect reliability guarantees, prioritisation levels and network resource utilisation. Such models will enable satellite operators to protect margins on mission-critical services while supporting scalable adoption across OEM portfolios.

Hybrid TN–NTN integration needs to shift from coexistence to co-ordination, meaning vehicles do not treat satellite and terrestrial connectivity as separate pipelines. Connectivity should be orchestrated dynamically, with seamless transitions across coverage environments and unified authentication, provisioning and management frameworks. To achieve this, operators must align roadmaps with 3GPP NTN standards and develop shared operational interfaces that support automotive deployments.

Industrialising satellite terminals for automotive-grade applications

Terminal strategy is another critical bottleneck in scaling satellite-enabled connected cars. While network capabilities and standards are progressing, hardware readiness, particularly for broadband applications, is not yet fully aligned with automotive manufacturing requirements.

OEMs operate on high-volume, cost-effective and tightly standardised production models. Components must meet stringent safety, durability and electromagnetic compatibility standards. Strict size, weight and power constraints are also in place.

Broadband satellite terminals, especially those designed for high-throughput applications, often struggle to meet these benchmarks. Antenna form factor, thermal management and integration complexity further complicate factory-fit deployment. These challenges make it more difficult to embed satellite connectivity as a scalable capability.

In contrast, narrowband solutions meet more of the requirements for automotive integration. Thanks to their lower power requirements, simpler architectures and alignment with evolving 3GPP NTN standards, they are more immediately compatible with SDV connectivity stacks. However, even narrowband solutions require more work on pricing models, compatibility across networks and a clear lifecycle support model to meet OEM expectations.

Addressing the terminal challenge requires a shift from technology demonstration to industrialisation. Satellite operators and hardware partners must prioritise cost reduction through scale, design for automotive form factors from the outset and pursue early engagement with regulators and OEM engineering teams. Pre-certified modules, reference designs and standardised integration pathways shorten the adoption cycle.

Connected cars present a chance to capture value, and the next 10 years will see a shift in the ecosystem as operators try to secure this opportunity. This shift relies less on satellite capacity and more on stringent alignment with OEM roadmaps, the evolution of sustainable and service-aware business models, and the industrialisation of automotive-grade terminals. Regulatory frameworks and consumer expectations will further shape how quickly satellite connectivity becomes embedded rather than optional. Operators that close the integration gap across networks, business models and hardware will be best positioned to turn connected cars into a sustainable long-term vehicle for growth.

Analysys Mason’s Satellite Mobility research programme examines how satellite operators, OEMs and ecosystem partners can unlock scalable growth in mobility markets. Our recent reports, Connected vehicles via satellite: worldwide trends and forecasts 2024–2034, Satellite-enabled basic emergency and location sharing in cars: consumer survey and Unlocking the satellite-enabled connected cars market, provide detailed market sizing, consumer insights and actionable strategic recommendations. For more information, please contact Sukhraj Kaur.

Download

Article (PDF)Author

Sukhraj Kaur

AnalystRelated items

Article

Satcom operators can turbocharge the space economy through launches, pricing and partnerships

Article

Satellite operators becoming manufacturers will benefit from SaaS, despite market fragmentation

Podcast

Predictions for the space industry in 2026