Mobile operators should deploy Open RAN small cells from neutral hosts to densify 5G networks

"MNOs should invest in small cells that are vRAN/Open RAN-compliant or capitalise on infrastructure from neutral hosts to strengthen the business case for 5G network densification."

The increasing congestion of mid-band spectrum in usage hotspots, and its poor indoor penetration, are reviving operators’ interest in deploying small cells to improve the quality of experience (QoE) for users and target new revenue streams. However, the business case for small cells has traditionally been limited by high costs and risks relating to overbuilding. Mobile network operators (MNOs) could optimise the business case for 5G small-cell densification by using virtualised/open RAN architecture and sharing infrastructure with neutral hosts.

MNOs are showing a renewed interest in small cells to improve coverage and to target enterprise opportunities

Small cells are compact radio access nodes that can be used to deliver additional capacity or coverage in areas of high traffic or low reception. Per node, they have significantly lower cost and power requirements than macro base stations, and are usually deployed to provide private or public connectivity in locations where macro sites struggle to deliver the required coverage or capacity.

Following the launch of 5G in 2019, the small-cells market slowed down. MNOs were allocated a large amount of new spectrum in 5G and the deployment of new mid-band equipment at macro sites became the priority to increase network capacity in areas where traffic volumes were high. However, because mid-band spectrum has reached higher penetration levels in areas of high traffic, MNOs are renewing their interest in network densification to augment capacity. Another motivation is to improve in-building QoE, which can be limited by the propagation challenges of mid-band airwaves.

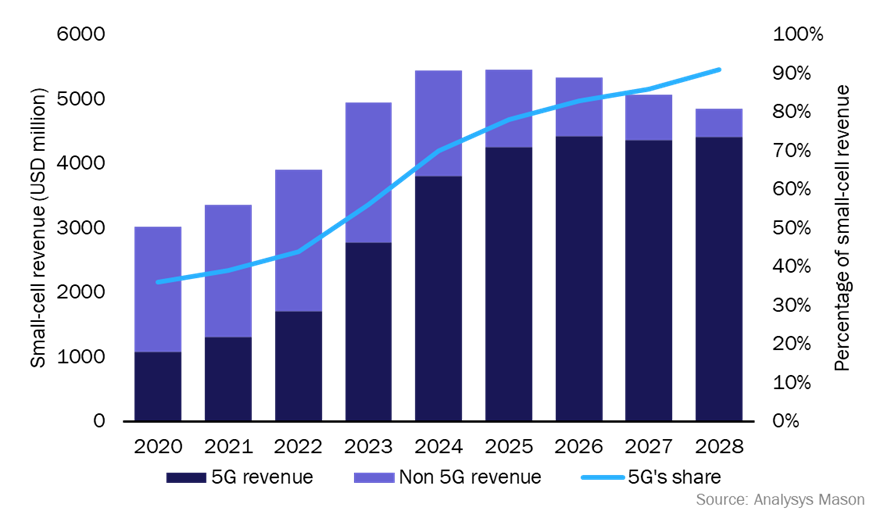

Analysys Mason’s latest forecast shows that revenue in the small-cells market increased at a CAGR of 18% between 2020 and 2023.

Figure 1: Small-cell revenue by type and 5G’s share, worldwide, 2020–2028

Network densification using small cells in public networks continues to be driven by increased traffic from 5G mobile broadband users, as well as operators’ desire to differentiate their mobile broadband offerings by enhancing QoE. Demand from B2B mobile broadband and emergency services has also been increasingly important to public network small-cell growth. For example, government funding has increased in recent years for small-cell projects that bring critical communications coverage for emergency responders.

Enterprise networks account for over two-thirds of small-cell deployments. Private networks represent a significant opportunity for small-cell vendors; total network spending is expected to increase at a CAGR of 48% between 2022 and 2028. As the adoption of 5G standalone (SA) networks increases between 2025 and 2028, operators could also offer hybrid public–private network services using small-cell deployments.

MNO investment in small cells is limited by capex fatigue, ROI concerns and the risks relating to overbuild

Small cells could help operators to improve QoE and address new enterprise opportunities, but the following factors continue to limit their investment in small-cell deployments.

- Capex fatigue. Many MNOs are experiencing capex fatigue from significant 5G macro network investment, which has so far not delivered a substantial ROI. This fatigue can make MNOs hesitant to invest further in 5G, especially as densification may involve large numbers of cells with high overall cost.

- Immaturity of use cases. MNOs are typically risk-averse and will not invest in small-cell infrastructure if ROI is unclear. While enterprise use cases and hybrid networks could offer opportunities for operators, many of these applications remain immature and underdeveloped. They could also require significant investment in 5G SA to provide additional functionality such as network slicing.

- Risk of overbuild. As well as being uncertain on the ROI of their own small-cell deployments, MNOs fear that other MNOs may also build out small-cell infrastructure in the same area, leading to competition for services. This would significantly diminish network monetisation opportunities from these deployments and weaken the overall business case for small-cell investment.

MNOs can optimise the small-cells business case by adopting Open RAN and neutral host infrastructure

MNOs should consider virtualised or Open RAN architecture, and neutral host infrastructure models, as two ways to reduce the costs and increase the flexibility of small-cell deployments, thereby optimising the business case and reducing the risk of investment.

Open RAN is expected to gain significant traction in the small-cells market and can bring a range of benefits to operator deployments. The virtualisation of the RAN allows for improved management, observability and agility within the small-cells network, enhancing QoE and efficiency. vRAN also supports flexible deployment of network functions, in the central cloud or on-premises. Cloud platforms can be attractive to operators and enterprises because they allow for centralised and scalable deployments, potentially reducing the physical space needed on-site. The introduction of open interfaces can enable the use of multiple vendors, which could improve product choice for deployers and customers, allowing them to choose the optimal combination of vendors and products for their use-case or spectrum requirements.

MNOs can also leverage small-cell infrastructure from neutral hosts to help to reduce costs and the risks of overbuild. Neutral hosts are companies that deploy sites, fibre and sometimes the active cells themselves and lease this infrastructure to operators. Capex-fatigued MNOs can use this approach to achieve network densification for enhanced coverage and capacity without major capex investment. Neutral hosts are also ideal candidates to facilitate network sharing between multiple operators, reducing the cost of network deployment per operator.

By adopting either Open RAN, or by leveraging neutral host deployments, operators can improve the business case for small cell coverage. However, the two concepts are even more effective when combined. Open RAN can maximise flexibility in neutral host deployments, allowing for greater interoperability between different tenant operators’ active networks (which may be supplied by different vendors) and the neutral host infrastructure. Therefore, by actively pursuing and supporting Open RAN that is enabled or even fully deployed by neutral hosts, operators could maximise the business case for further small-cells coverage.

Article (PDF)

Download