Telcos, it's time to dial up your space strategy

“A satellite partnership is a start, but without a joined-up space strategy telcos risk having the next era of connectivity defined for them.”

10 years ago, the satellite communications sector lagged well behind mainstream telecoms in maturity and development. Then, in December 2015, SpaceX returned a booster to its launch pad for the first time, ready to fly again. Overnight, the cost of access to space dropped by two thirds, opening the door to a new wave of space technologies.

The decade since has been a period of radical change. Space communications have not merely kept pace with the wider telecoms industry; in several dimensions they have leapfrogged it. Analysys Mason research data on direct-to-device (D2D) services shows that 68 operator groups around the world now have active partnerships with at least one satellite player.

But a partnership is not a strategy. And for most telecoms operators (telcos), that deeper work has not yet begun. What most organisations are missing is a space strategy that brings commercial, technical and regulatory functions together around the same goals.

Space is already woven into the fabric of global connectivity

Space connectivity is accelerating – and it may scale far faster and further than most operators currently assume. It is already a native component of the 5G standard handset and will be a baseline capability in 6G devices. Analysys Mason research has found that over 90% of consumers are interested in at least one type of satellite D2D service.

Regulatory filings to secure rights for planned constellations have rapidly expanded in size and scope. The size of those future constellations that satellite operators are seeking to deploy has increased by orders of magnitude in just a few years. The SpaceX initial public offering (IPO), expected in June 2026 and likely to be one of the largest in history, will pull further capital into the sector at speed. Where will this trajectory lead? Whether Starlink’s infrastructure ends up ten, or even a hundred times larger than it is now, the competitive dynamics for every operator in this industry will look different.

Space services are becoming embedded more deeply in every corner of industry: from critical infrastructure to remote operations in mines, aircraft or vessels; in global supply chains, climate tracking, and monitoring of all our activities on Earth.

For telcos, that pervasiveness is both the opportunity and the challenge. Space communications does not extend the existing network; it expands what a network can fundamentally be and where it can reach.

The operators that grasp this earliest will define the boundaries of the next generation of connectivity. Those that do not will find those boundaries drawn for them.

Partnerships are underway; strategy is not

Most operators are approaching space the way they approach any emerging opportunity: with one toe in the water. That is understandable, as the technology is still maturing and the competitive dynamics are unsettled. Early partnerships are a sensible way to learn without overcommitting, but the time to decide more structural inclusion is closer than many operators think.

The default position for most telcos is to look at space through the lens of coverage: a way to reach places where terrestrial infrastructure cannot serve customers at a viable cost. That has been the satellite value proposition for decades. This vision, however, does not reflect the change in economics, long-term competitive positioning or customer value.

Telcos should now explore the following questions:

- Should mobile operators own D2D infrastructure or not?

- To what extent should they control the service?

- If a satellite player with structurally lower costs can serve specific areas more efficiently, what happens to the value model?

Some operators have already challenged the default position by taking direct investment positions in D2D, such as Verizon and Vodafone in AST SpaceMobile.

For fixed and cable operators, the risk of subscriber loss is already arriving at the edges of their networks, as mega constellations are closing the speed and price differential faster than anticipated.

Tower companies are exposed too. Their concern is structural: if mobile operators reconfigure their edge networks as D2D coverage matures, the demand that underpins tower valuations may also be affected. American Tower took a direct position in space infrastructure and did not wait to see how mobile operator decisions would play out.

None of these risks are addressed by a tactical commercial partnership. Telcos that stop here will find themselves reacting to a market they had no hand in defining.

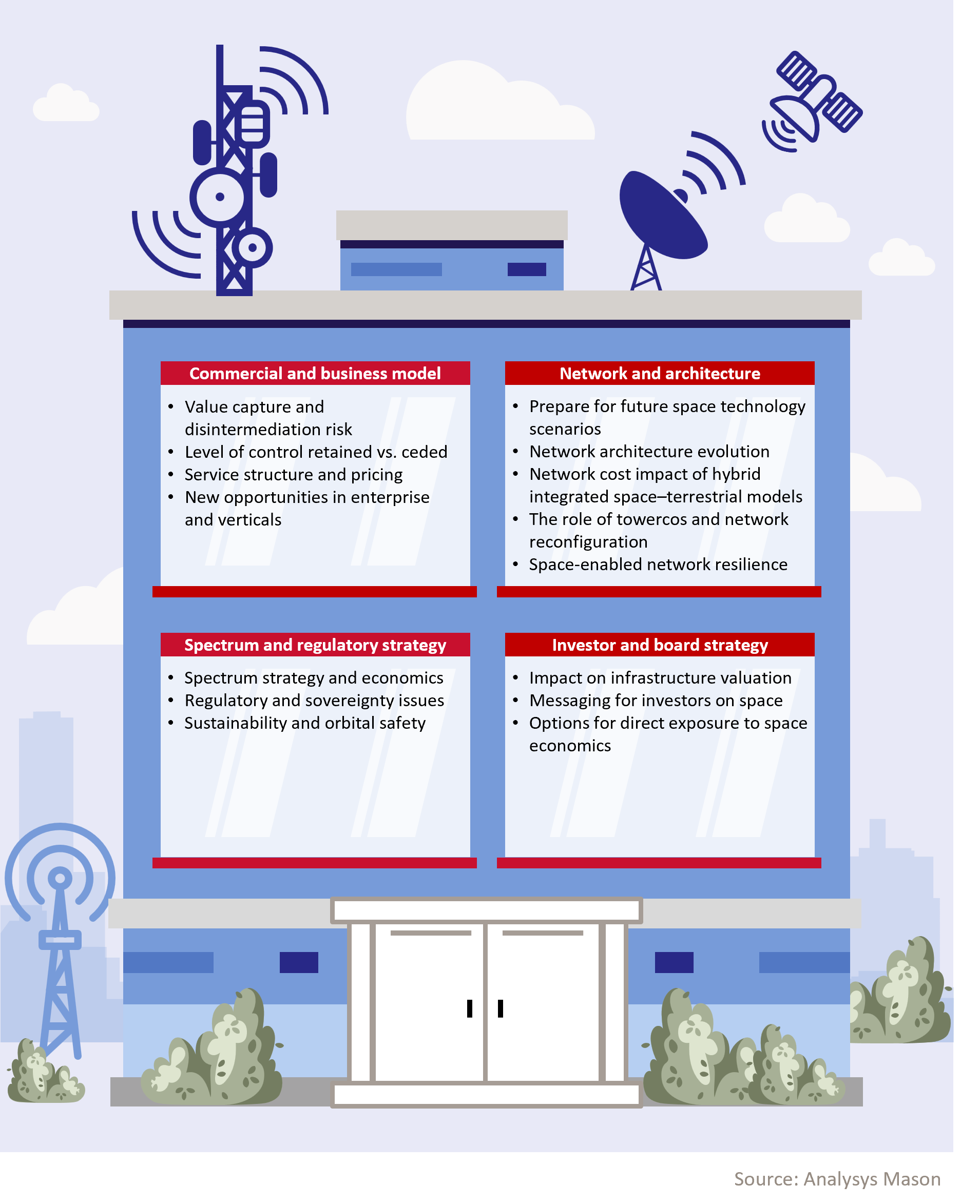

Strategic questions every telco needs to answer

Space is already on the agenda for most telcos – across technology, commercial and regulatory domains – but without a shared strategy, the sum could be less than its parts. In our experience, misalignment between functions is one of the most consistent and avoidable sources of strategic failure, and could lead to telcos not capturing the bigger opportunity.

For leadership teams that are serious about turning a first partnership into a strategy, there are questions that need to be asked across multiple dimensions of the business.

Figure 1: Strategic questions that every telco needs to answer

Structural shift rewards early movers

Telcos have seen structural changes before: the move from digital subscriber line (DSL) to fibre, telco–media convergence and the arrival of streaming, and the economics of mobile data. In each case, the structural shift was visible before it became inevitable. The operators that moved early did not merely capture more revenue; they acquired influence over how the new ecosystem would be structured and ultimately had a stronger long-term position.

Space is following the same trajectory. What is visible today, including the first non-terrestrial network (NTN)-enabled devices, the first video calls from space, the early partnerships, constellation filings running into millions of satellites, and billions being invested, are the initial telltale signs of what this could look like in 5 to 10 years. The operators who will shape that ecosystem and the ones with a deeper strategy now, stand to benefit the most.

The combination of telecoms and space economics and telecoms and space technology is not straightforward. Mistakes will be expensive. The decisions operators take – on network architecture, on partnerships, on how much of the value chain they choose to own – will be difficult to reverse once the ecosystem has settled around them. Telcos need to decide now what meaningful role they want to play in space and how to best position themselves.

Develop your space strategy with specialist expertise

Expertise across telecoms and space is rare. Analysys Mason delivers both. In the past 2 years, we have completed more than 30 satellite and space projects, advising operators, investors and regulators on the decisions that will shape this sector for the next decade.

We work with clients from early-stage ideation and strategy development, through cross-functional co-ordination across commercial, technical, network and regulatory teams, to transformation and execution.

Operators and investors considering their space strategy should be talking to us now. Get in touch with Antoine Grenier and our space team.

Author

Antoine Grenier

Partner, space and satellite, Consulting leadRelated items

Article

Take-private deals are reshaping digital infrastructure, while space companies look to IPOs to support growth

Article

Regulators should define clear spectrum rules to foster innovation in satellite D2D

Article

Government demand is accelerating the shift towards satellite as a service in Earth observation