Operators’ spending on vendor IoT device management platforms will reach USD263 million by 2026

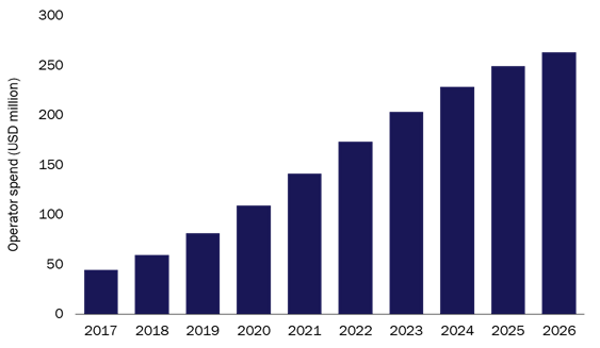

Operators want to offer IoT device management platform capabilities, but most lack the credibility and resources to build their own platforms and compete in the market. Most operators therefore rely on vendor platforms to complement their IoT offerings. We expect that operator spend on vendor platforms will grow from USD44 million in 2017 to USD263 million in 2026.

This article is based on Analysys Mason’s report IoT forecast: operator spend on device management platforms 2017–2026. This report analyses the key trends, drivers and challenges in operators’ adoption of IoT device management platforms and provides recommendations for vendors in this market.

Most operators are not well-equipped to compete in the IoT device management market and prefer to rely on vendor partners

Many operators want to expand and support their IoT businesses beyond connectivity by offering IoT platform services such as device management. However, they have limited skills and experience in building and providing such platforms. Most operators are also reluctant to commit to developing such technologies and wish to avoid competing directly with web-scale players such as AWS and Microsoft Azure which are known to respond faster to platform technology and market development.

Many operators are using third-party device management platforms from vendors such as Software AG and Telit to develop a market presence beyond connectivity (Figure 1 provides some further examples of operator and vendor platform partnerships). Operator spend on vendor platforms is expected to continue to grow with a CAGR of 22% to reach USD263 million by 2026 (Figure 2).

Figure 1: Examples of operators using vendor IoT platforms with device management capabilities1

| Operator | Technology provider | Platform | ||

|---|---|---|---|---|

|

Bell |

|

Sierra Wireless/Numerex |

|

nxFAST IoT platform |

|

Etisalat |

|

Software AG |

|

Cumulocity |

|

Polkomtel |

|

AVSystem |

|

Coiote IoT platform |

|

Sprint |

|

myDevices |

|

Cayenne |

|

StarHub |

|

Nokia |

|

IMPACT |

|

Swisscom |

|

Telit |

|

deviceWISE |

|

Tata Communications |

|

HPE |

|

Universal IoT platform |

|

Telenor Norway |

|

Cisco |

|

Cisco Kinetic |

Source: Analysys Mason, 2018

Figure 2: Operator spend on vendor IoT device management platforms, worldwide, 2017–2026

Source: Analysys Mason, 2018

A number of other significant operators such as AT&T and Verizon have invested in building their platform capabilities beyond connectivity and aim to establish industry recognition without forming vendor partnerships. Within their respective markets, such operators have the capacity and commitment to continue supporting their platform businesses. However, connectivity remains their core strength, and to attract platform customers, they need to match competitors’ platform technologies and/or offer competitive pricing.

To attract operators, vendors need to show a strong commitment to the development of IoT device management technology

Platform providers that wish to partner with telecoms operators should demonstrate their ability to augment operators’ IoT offerings and remain competitive in the market. Vendors’ solutions must fulfil the following requirements.

- They must build on the operator’s core business and integrate easily with it. Operators want to offer device management as an extension to their connectivity services. As such, vendors should simplify the integration of their platforms with operators’ current systems. This may include identifying feature overlaps between their platforms and operators’ existing systems and resolving issues that may occur upon integration. Additionally, providing modular platforms helps operators to flexibly customise service bundles and prices to meet different customer needs.

- Solutions should offer significant ecosystem and channel-to-market advantages. Operators are interested in vendors that can offer additional market support and services on top of their technologies. Forming partnerships with vendors that are visible and established in markets such as agriculture, manufacturing and healthcare can help operators to gain momentum in these markets. An example is GE Digital’s support of AT&T, Deutsche Telekom and China Telecom in the industrial IoT market.

- Vendors’ platforms should have a responsive approach to market dynamics. The IoT device management platform market is evolving and is influenced by several factors including challenges such as security and service quality concerns and opportunities such as the emergence of related technologies including artificial intelligence and blockchain. Operators need agile partners that respond rapidly to technology and market developments. For example, IoT platform start-up Evrything has added support for blockchain and augmented reality to its platform and has expanded into Asia–Pacific since October 2017 in response to market trends.

Vendor partners that offer comprehensive and advanced device management platforms allow operators to focus on differentiating their role in the IoT applications and services markets across different verticals.

1 For more information, see Analysys Mason’s IoT platform contracts tracker.

Downloads

Article (PDF)Latest Publications

Article

If Vodafone IoT is a success as an independent firm, other operators will also spin off IoT divisions

Forecast report

Italy: wireless IoT market trends and forecasts 2023–2032

Forecast report

Sweden: wireless IoT market trends and forecasts 2023–2032