Europe’s fibre problem is no longer coverage, it is conversion

20 May 2026 | Strategy, Transaction

Article | PDF | Digital Infrastructure | Raising finance | Rural broadband

“Europe has spent billions building fibre. The harder question now is whether operators can persuade customers to use it.”

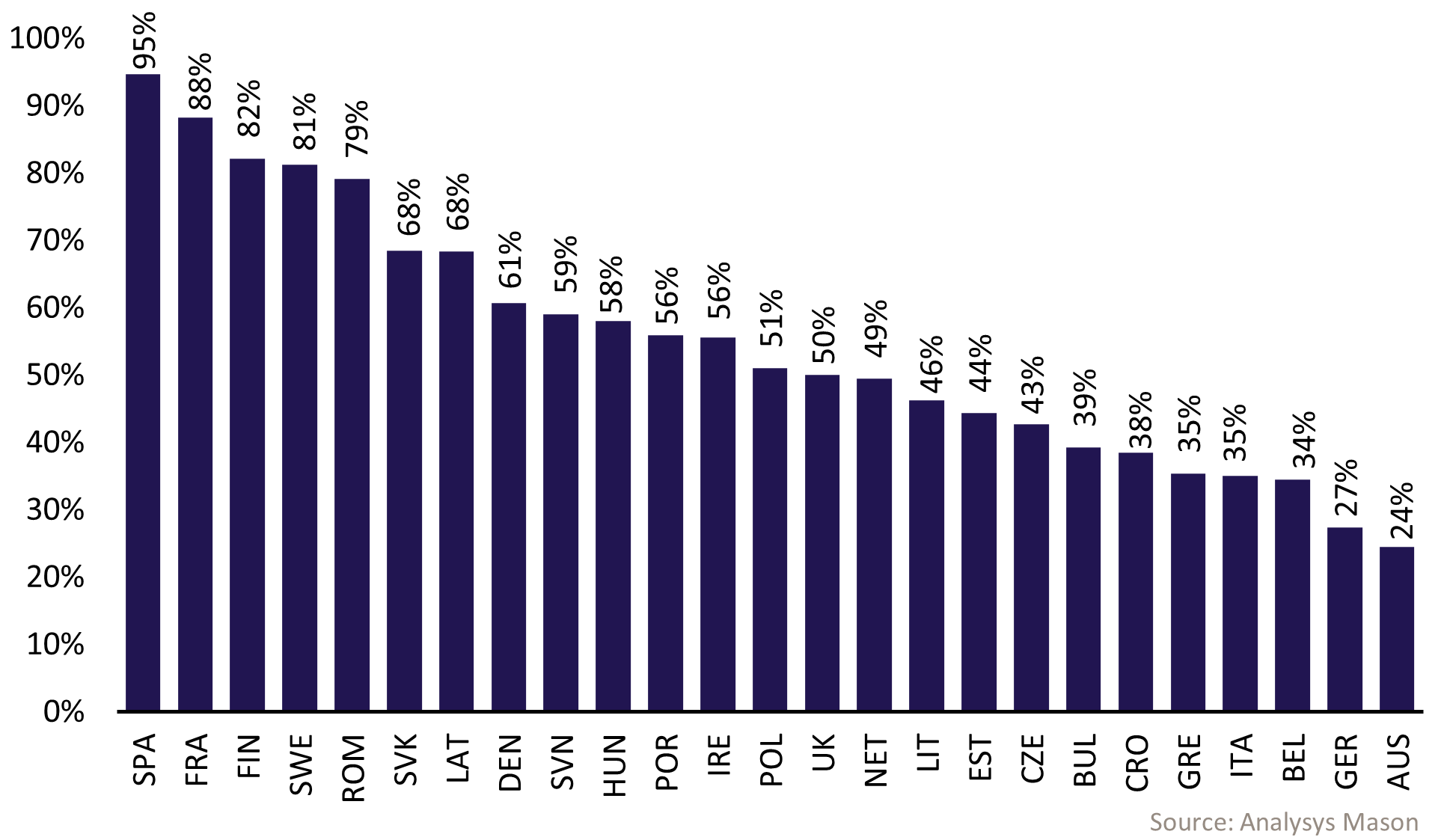

Europe has built the fibre networks investors asked for, but in too many markets customers have not followed. Spain and France convert coverage into customers with ease, whereas Germany and Italy do not to the same extent (see Figure 1). For investors, this means coverage milestones are no longer enough to prove the investment case. Our experience advising on fibre strategy, commercialisation and take-up across Europe provides insight into the factors behind these disparities and how to address them.

Figure 1: Fibre-to-the-home (FTTH) take-up by country (EU24+UK,1 end of 2025)

The first wave of FTTH deployment in Europe was driven by a clear supply logic: expand coverage, displace copper and rely on superior performance to drive adoption. In several markets, this logic worked. Where fibre arrived early, while copper was still the dominant access technology, the performance gap was obvious and adoption followed quickly.

However, across much of Europe, the competitive landscape evolved differently. Fibre-to-the- cabinet (FTTC) and cable DOCSIS networks were upgraded aggressively and reached mass-market scale before fibre. These technologies delivered speeds and reliability that were ‘good enough’ for the majority of households. As a result, when FTTH finally reached scale, it did not replace an inadequate product, but a satisfactory one.

The hidden power of substitution

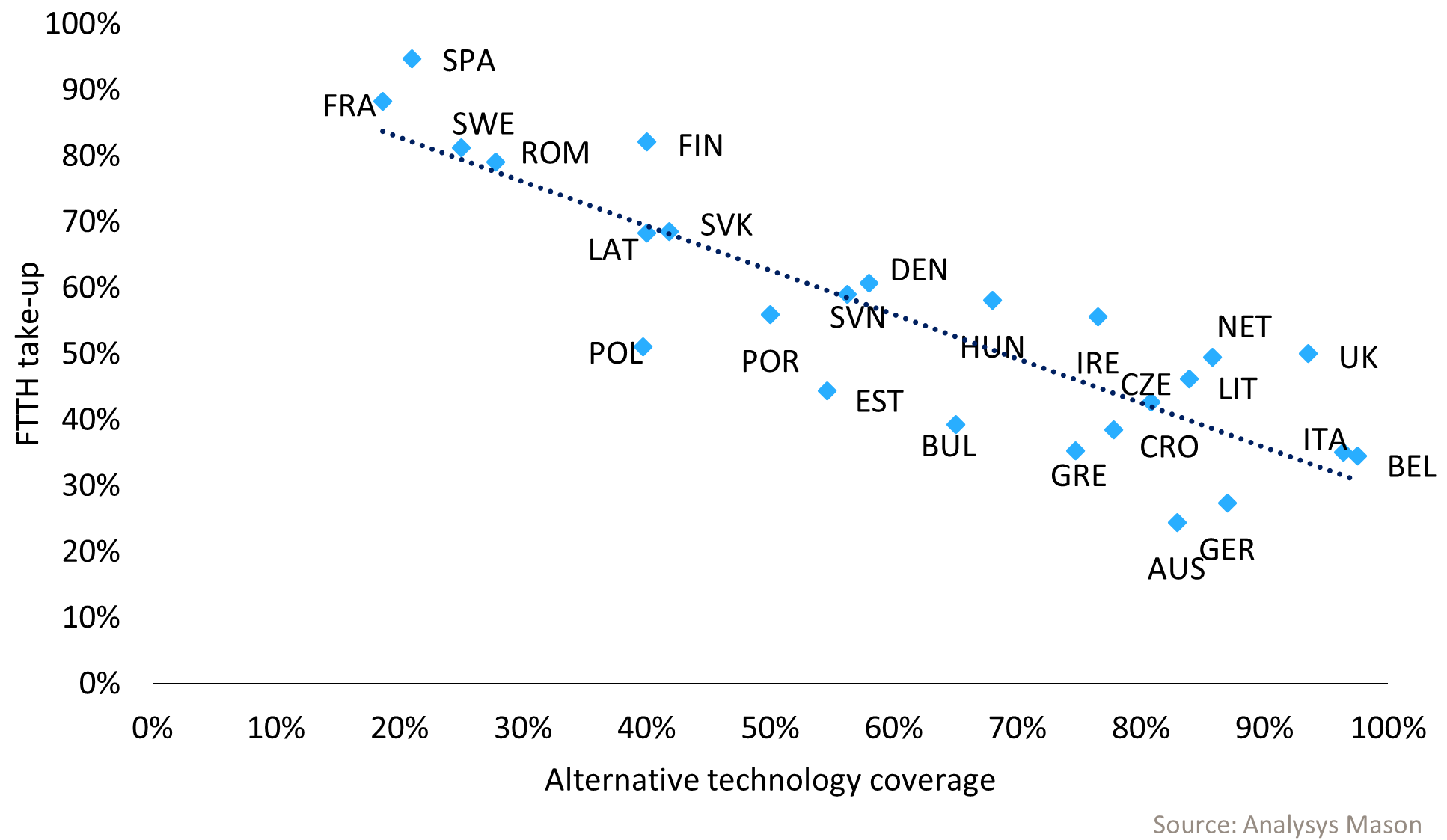

A consistent pattern emerges when FTTH adoption is compared with the availability of alternative access technologies (see Figure 2). Markets with extensive FTTC and DOCSIS coverage tend to show systematically lower fibre take-up, regardless of income levels, regulatory regimes or market structures. The presence of credible substitutes dampens demand for FTTH.

Figure 2: Correlation between FTTH take-up and alternative technology coverage (EU24+UK,2 end of 2025)

This is not a technology issue, but a behavioural one. Consumers do not buy the ‘best’ product in absolute terms. They buy the product that satisfies their needs at the lowest perceived cost, effort and risk. When existing broadband already supports streaming, gaming, remote work and smart-home use cases, additional speed or lower latency offers diminishing perceived value, unless there is a clear price advantage.

This helps explain why countries with similar fibre footprints show markedly different take-up levels. Coverage answers the question, “can I buy fibre?”. Take-up answers a different one: “do I feel the need to switch?”.

In economic terms, fibre has moved from a disruptive to a sustaining innovation. For many households, it no longer solves a new problem; it simply improves a service they already feel is good enough. In this context, the friction associated with switching – installation, uncertainty and contractual constraints – can outweigh the perceived performance gains.

This dynamic is not unique to telecoms. Many technology markets follow a similar trajectory. Products compete first on performance, then reach a point where they exceed what mainstream users can meaningfully use. Beyond that point, adoption slows and differentiation shifts away from raw capability.

Operators must stop selling speed and start selling reasons to switch

If performance is no longer enough, retail strategies must evolve. The markets that are closing the take-up gap are those that have stopped selling fibre as ‘more speed’ and started selling it as ‘different value’. What ‘different value’ means in practice depends on who you are and where you operate: retail versus wholesale economics, and urban versus rural demand dynamics, imply very different levers to stimulate switching.

Four value factors matter when trying to increase fibre take-up:

- Status and quality. In high-performing markets, fibre is increasingly positioned as a marker of quality and modernity, not a technical upgrade. Visibility, exclusivity and brand association matter more than headline Mbit/s. Fibre becomes a signal of a better connected home, not just another utility.

- Convenience over capability. Customers rarely articulate demand in terms of latency or throughput. They care about reliability, simplicity and not having problems. Removing friction across the entire journey – ordering, installation, in-home wiring, customer care – often creates more perceived value than another speed tier.

- Bundling that feels relevant. FTTH adoption accelerates when bundled with services that customers already value: premium TV content, mobile plans, home security, cloud storage or emerging AI-enabled services. Bundles shift the conversation from “why switch?” to “why not?”.

- Migration incentives. Regulation can tilt the balance. Favourable wholesale pricing of the incumbent, clear copper switch-off roadmaps in selected areas, and policies that reduce the attractiveness of legacy platforms all help shorten the overshoot phase and strengthen migration incentives.

The good news is that low take-up today does not imply a structural ceiling. Forecasts suggest that countries currently lagging can still experience substantial growth by the end of the decade, provided demand dynamics are addressed.

However, value is no longer driven by coverage alone. For investors, the key question is not “how fast can we build?”, but “how effectively can the ecosystem stimulate switching?”. This shifts the focus from build-out milestones to commercial execution. The key is no longer just having coverage, but having a credible and defensible story for how that coverage is converted into customers.

In an environment of heightened lender scrutiny and margin pressure, this commercialisation narrative becomes central to financing resilience during the hold period and to securing the right type of return at exit:

- investors should assess the robustness of the commercialisation plan with the same discipline applied to the deployment plan

- the investment case should show not only where fibre has been built, but why customers will switch.

For retail operators, the challenge is to redesign propositions around perceived value, not technical superiority:

- identify the specific barriers to switching

- translate these insights into differentiated, value-led propositions

- communicate a clear, simple and compelling reason to switch beyond ‘more speed’.

Our experience supporting investment cases, refinancing decisions and exit planning in digital infrastructure suggests that the next phase of fibre value will be won by those that can turn coverage into customers. Analysys Mason works with operators, investors, lenders and digital infrastructure providers to assess fibre take-up risk and identify practical ways to turn coverage into customers. To understand how these dynamics apply in your market, speak to our fibre and broadband strategy experts.

1 Excludes Malta, Luxembourg and Cyprus.

2 Ibid.

Article (PDF)

DownloadAuthor