Satellite operators becoming manufacturers will benefit from SaaS, despite market fragmentation

04 February 2026 | Research and Insights

Article | PDF (3 pages) | Defence and Sovereign Space| Earth Observation| Emerging Space Applications| Satellite Broadband| Satellite Capacity| Satellite D2D| Satellite Manufacturing and Launch| Satellite Mobility| Satellite Networking Technologies | Space

"The satellite-as-a-service model brings new opportunities to satellite operators, but presents a risk of market cannibalisation."

The satellite-as-a-service (SaaS) model has been growing in popularity over the last few years; numerous contracts and funding announcements have cited it as innovative and advantageous for satellite manufacturing. However, the term ‘SaaS’ is often poorly defined, and is used to incorrectly refer to a number of different models, thus leading to confusion.

Satellite manufacturing will generate USD667 billion in cumulative revenue worldwide between 2024 and 2034. Satellite operators and manufacturers must evaluate how they can use the SaaS model to capture some of this revenue and should consider what challenges may lie ahead that would prevent them from outpacing their competition and benefitting from the advantages that SaaS offers.

The SaaS model will work best when selling to new satellite service customers

When following the SaaS model, a vendor must both manufacture and operate the satellite; the customer only has access to the satellite data. This lowers the barriers to satellite market entry for these customers because it requires less of an initial investment in areas such as personnel, expertise and ground station facilities. However, it also means that a single provider is used for all manufacturing and operations, which could limit customers’ ability to make changes or develop their own expertise. As such, this model is most suitable for customers that are aiming to enter a new market or expand satellite services to their existing network.

Some satellite operators are now starting to sell satellites alongside data

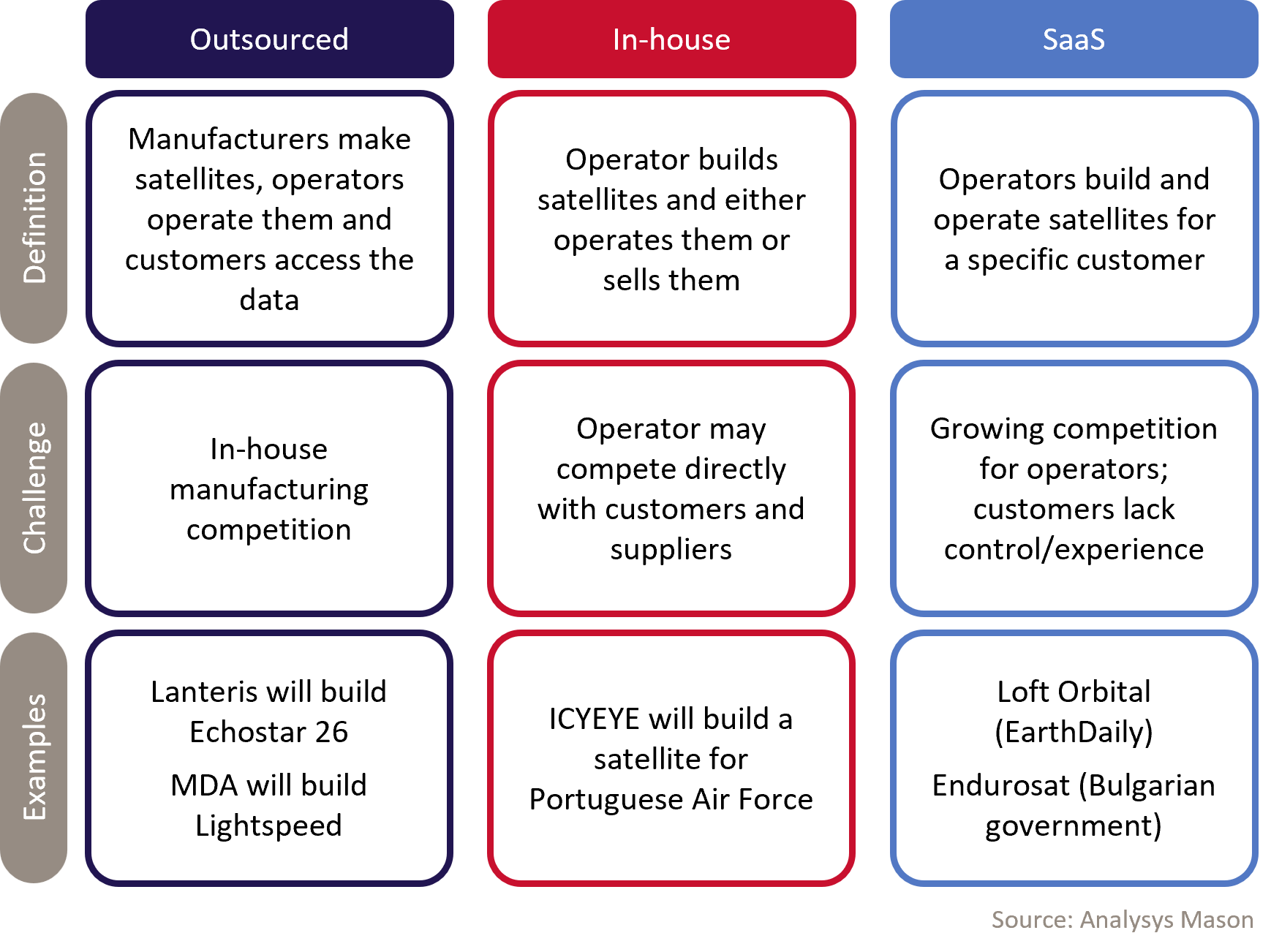

We have observed a shift in the satellite manufacturing landscape in the past few years. Traditionally, satellite manufacturers, satellite operators and service users have played distinct roles, but players are now expanding their capabilities, leading to models where offerings become more mixed. This can be seen in Figure 1.

Figure 1: Shift in the satellite manufacturing landscape

The first step has been for operators to move to the ‘in-house model’. In this model, operators manufacture their own satellites. This gives them the opportunity to build and sell satellites for customers to operate themselves, as is the case with ICEYE’s deal with the Finnish Defence Forces and Planet’s agreement with SKY Perfect JSAT. Earth observation (EO) constellations are strongly driving this shift. Indeed, EO manufacturers were moving towards service-based offerings such as with the MDA and Canadian government’s RADARSAT programme, long before geostationary-orbit (GEO) communications players started to offer satellite leasing, such as seen recently with SLI and AscendArc.

The main benefit of this shift for satellite operators is to increase competitiveness, control more of the satellite manufacturing process and provide a more end-to-end offering. The key disadvantage was previously the cost of expanding into satellite manufacturing. However, as the line between offerings blurs, there is also growing potential for competing with oneself and one’s customers, and sacrificing long-term relationships for short-term opportunities.

In-house manufacturing strengthens operators’ ability to tailor their constellations but decreases the addressable market

Some operators have gone one step further due to pressures for rapid scaling; they have adopted the SaaS model and manufacture their own satellites in house, to both serve their own requirements and gain new customers. Bringing the manufacturing process in-house allows operators to have more control over the process, engage with hardware-focused investors, tap into revenue growth opportunities and further differentiate themselves in the market. We estimate that 44% of all constellations currently in deployment are manufactured by satellite operators in house. However, satellite manufacturing remains an expensive process that requires specific expertise, personnel and facilities. Operators that become manufacturers may assume more control over the process, but also take on more risk and capital.

This pivot can yield a stronger market position, but these providers may find that customers want to buy and operate satellites themselves, thus reducing the demand for their services. Similarly, some customers may also be tempted to become manufacturers. This will lead to market fragmentation and potential oversupply, which will challenge overall market growth.

It will also increase the competitive pressure on traditional satellite manufacturers, who will experience declining demand due to competition from previous customers.

Government sovereignty requirements will threaten SaaS models, unless vendors establish local capabilities

The demand for satellite access/control among government end users is growing due to sovereignty concerns. There is a growing push for regional representation in Europe, which is why companies such as ICEYE have successfully sold satellites to several European governments. Manufacturers and operators can use SaaS to satisfy these customers; it offers exclusive access while leaving the development, deployment and day-to-day operations to the former players. However, the push for sovereignty can also lead to a need for more national, domestic suppliers, as seen in Italy with the project between the Italian government and Leonardo. This trend is expected to increase with rising levels of geopolitical tension.

This push will also close off markets to foreign players. As such, Analysys Mason advises that satellite manufacturers and operators that wish to expand their role or move into specific territories make strategic mergers and acquisitions to provide a sovereign solution to government customers.

There is no ‘one-size-fits-all’ solution; vendors and customers must be aware of the strengths and weaknesses of each model to make the choice that best fits their needs.

For more insight, data and strategic analysis regarding satellite manufacturing, see Analysys Mason’s Satellite constellation build and launch strategies and Earth observation satellite constellation strategies, as well as ongoing research in the Satellite Manufacturing and Launch and Earth Observation research programmes.

Article (PDF)

DownloadAuthor

Dallas Kasaboski

Principal Analyst, expert in space infrastructureRelated items

Article

Strategic ecosystem alignment will fuel growth in the satellite-enabled connected car market

Article

Satcom operators can turbocharge the space economy through launches, pricing and partnerships

Podcast

Predictions for the space industry in 2026