SpaceX is betting on open IoT standards

"SpaceX’s move towards standards-based IoT solutions in the direct-to-device market reflects the industry’s shifting landscape from proprietary solutions to standardisation."

SpaceX made its first-ever acquisition in August 2021 when it purchased Swarm Technologies, a start-up known for its early adoption of proprietary ultra-narrowband satellite IoT solutions; a move that signalled SpaceX’s intention to expand its capabilities and diversify its offerings to cater to a broader range of customers. However, Swarm’s announcement in July 2023 that it would cease selling new devices has raised eyebrows. Swarm’s decision appears to be directly linked to its parent company’s intention to shift the focus of its IoT strategy towards the direct-to-device/cell (D2D/C) market.

Why is this worth noting? In other verticals – specifically broadband access, enterprise, mobility, and government – that are using the Starlink offering, SpaceX is offering proprietary solutions, which has enabled it to scale rapidly. However, it would appear that integrating with telcos in the IoT market requires a different approach for achieving scale and success.

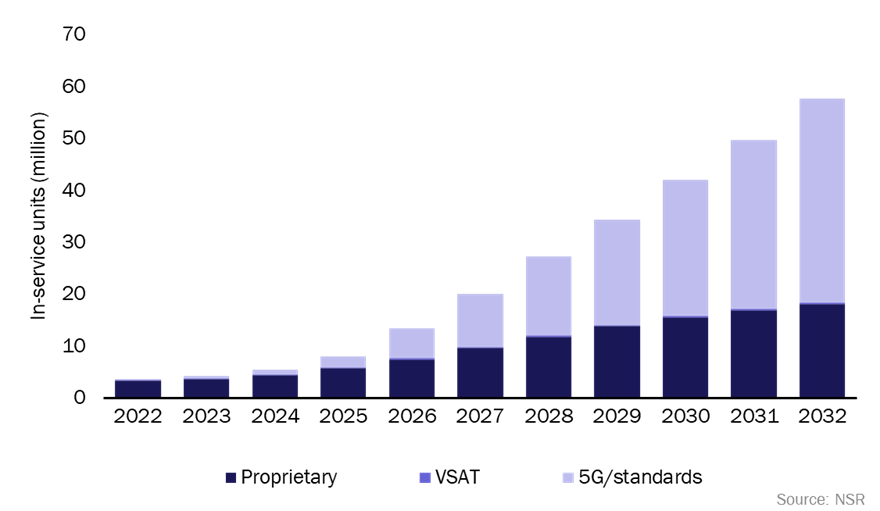

The move is not surprising to NSR, as this shift in direction towards standards-based solutions from proprietary ones aligns with the trend that was outlined in our recently released report, M2M and IoT via satellite, 14th edition report, that the number of in-service IoT units using 5G and standard-based protocols (for example, LoRa) is expected to grow rapidly in the next 10 years, reaching 39.3 million by 2032, out of a total market of 57.7 million devices (Figure 1).

Figure 1: IoT in-service units by technology type, worldwide, 2022–2032

The satellite direct-to-device ecosystem is taking shape … gradually

3GPP Release 17’s inclusion of non-terrestrial networks opens the door for direct-to-cell development, allowing IoT devices to communicate with satellite networks directly. Chipset manufacturers are working to integrate standards; for example, Mediatek has demonstrated its 3GPP NTN technology, and Qualcomm has launched new 3GPP modems. In March 2023, the FCC unveiled a proposed satellite direct-to-device regulatory framework, which will facilitate partnerships and collaboration between satellite operators and telecoms operators (telcos), as well as establish ground rules for market players. All these advances will promote the development and growth of the D2D ecosystem.

To seize the opportunities presented by this shift towards standardization, SpaceX has been forming partnerships with terrestrial network operators worldwide. Some recent examples include its partnership with T-Mobile to broaden coverage in the USA, and Optus for D2C coverage across Australia. These future integrations have primarily been marketed as opportunities for consumers to request emergency assistance and send text messages back and forth, but such partnerships are also ideal for narrowband IoT applications; these applications have a clear short-term value proposition for enterprises that crave 100% visibility on mobile assets.

One exciting prospect that could arise from SpaceX’s D2C vision is its potential to connect a wide array of devices and allow roaming to satellite networks, especially those that are mobile, moving in and out of terrestrial network coverage, like passenger vehicles. Elon Musk is known for his ambitious goals and SpaceX’s D2D initiatives could pave the way for connecting Tesla cars. Musk has previously noted that Tesla vehicles will not be line-fit to connect to the Starlink service, this was in the context of high-speed flat panel antenna connectivity – a much more expensive service to integrate into vehicles. Musk has since commented that SpaceX’s narrowband D2D initiative is much more suited to Tesla vehicles.

However, it is important to note that these partnerships will take time to actually implement. Bigger satellites are needed for this service, which in turn will need to be delivered by SpaceX’s larger Starship launch vehicle – the same one that was destroyed after a failed test flight in April this year. Consequently, SpaceX has not yet set a date for the satellite-to-cell service to be trialled, but it is likely to occur some time in 2024. In the meantime, other proprietary services are already moving in.

Proprietary solutions still have their place in the IoT ecosystem

From a technical perspective, there is no definitive conclusion as to which protocol strategy is better – using proprietary systems, 3GPP standards, or other standards-based systems such as LoRa. All have their advantages and disadvantages.

Proprietary protocols, whether deployed on small satellite constellations, or using leased mobile satellite service (MSS) capacity, do provide some advantages over standards-based protocols according to operators, which are mainly related to efficiencies and costs. Satellites can use highly efficient proprietary waveforms to handle billions of sensors on a single footprint, and therefore offer better economies of scale than current 3GPP standards.

This is in part due to the overhead in satellite-to-cellular and cellular-to-satellite hand-off on 5G 3GPP systems, which needs to be considered carefully, otherwise the data overhead could overwhelm networks. While 3GPP Release 17 improves this significantly, more needs to be done to make this a more seamless process. Some satellite operators are therefore already going beyond Release 17 in order to improve efficiency, and it is likely that such improvements will be incorporated into future releases.

For end users, deploying proprietary systems makes most sense when there is no terrestrial connectivity available (or it is just not needed), because the greater spectrum efficiency can potentially reduce the price down to single-digit dollars per year in some use cases.

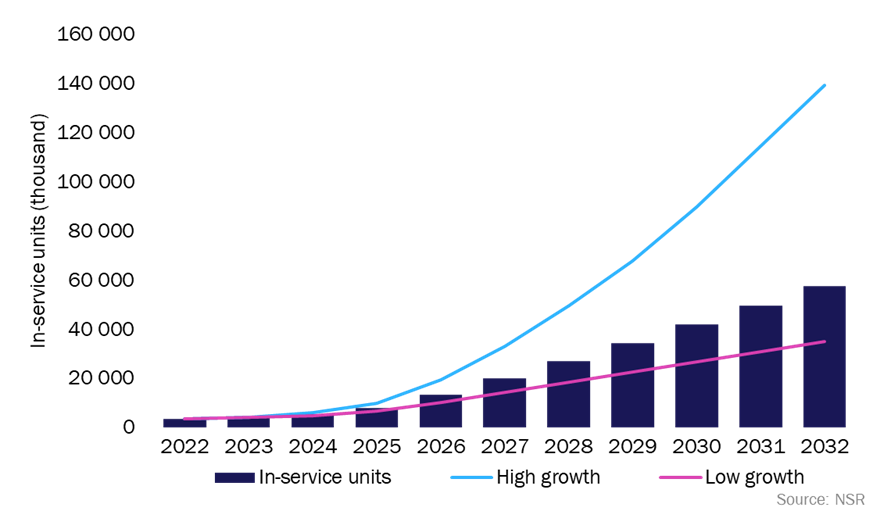

For standards-based IoT solutions though, operators will need to strike a balance between backward compatibility and performance and regulatory certainty. Collaborative network planning and integration are also essential to ensure seamless integration of networks. If stakeholders come together and co-operate in ecosystems based on standards, this could maximise synergies between terrestrial and non-terrestrial networks. If this occurs, and more roaming agreements come into place, a high-growth scenario for the broader satellite IoT market could occur, resulting in almost 140 million in-service units in 2032 (Figure 2).

Figure 2: IoT in-service units by scenario, worldwide, 2022–2032

Other uncertainties will challenge business models including the revenue split between satellite operators, MNOs, IoT service providers, and other value-chain members. Any regulations and policies will also introduce elements of uncertainty.

Bottom line

SpaceX’s move towards standards-based IoT solutions in the direct-to-device market reflects the industry’s shifting landscape from proprietary solutions to standardization. This strategic move should position SpaceX to take advantage of the rapidly growing direct-to-device IoT market of the future while aligning with industry standards and trends. SpaceX should be well-positioned to play a pivotal role in the direct-to-device market by forming partnerships, leveraging standards and capitalizing on decreasing device prices.

Although a lot of uncertainties remain in the D2D market, going by the open standards route would simplify telco integration and increase market penetration. At the moment, proprietary solutions have the edge; but 5G standards will begin to outpace growth and market penetration by 2028 and this will continue in the long term. This market development is still 4 years away, but SpaceX is making a bet today that open standards will win over proprietary systems.

Podcast: Why telcos need to develop a satellite strategy now

Article (PDF)

DownloadAuthors