Government demand is accelerating the shift towards satellite as a service in Earth observation

"Sovereign Earth observation programmes are rewarding vendors that can deliver secure, end-to-end capability rather than standalone data."

Government and military customers are the foundation of demand in the Earth observation (EO) market: they consistently drive spending through their requirements for defence intelligence and surveillance. This dominance is reflected in EO investment patterns, and Analysys Mason’s Earth observation news and deals: trends and analysis 2H 2025 shows this dependence deepening.

Heightened geopolitical tensions are prompting states to expand their national monitoring capabilities, accelerate procurement cycles and secure guaranteed access to EO data. This is driving increased demand for sovereign access to EO data and analytics as governments prioritise domestic capability and secure data pipelines.

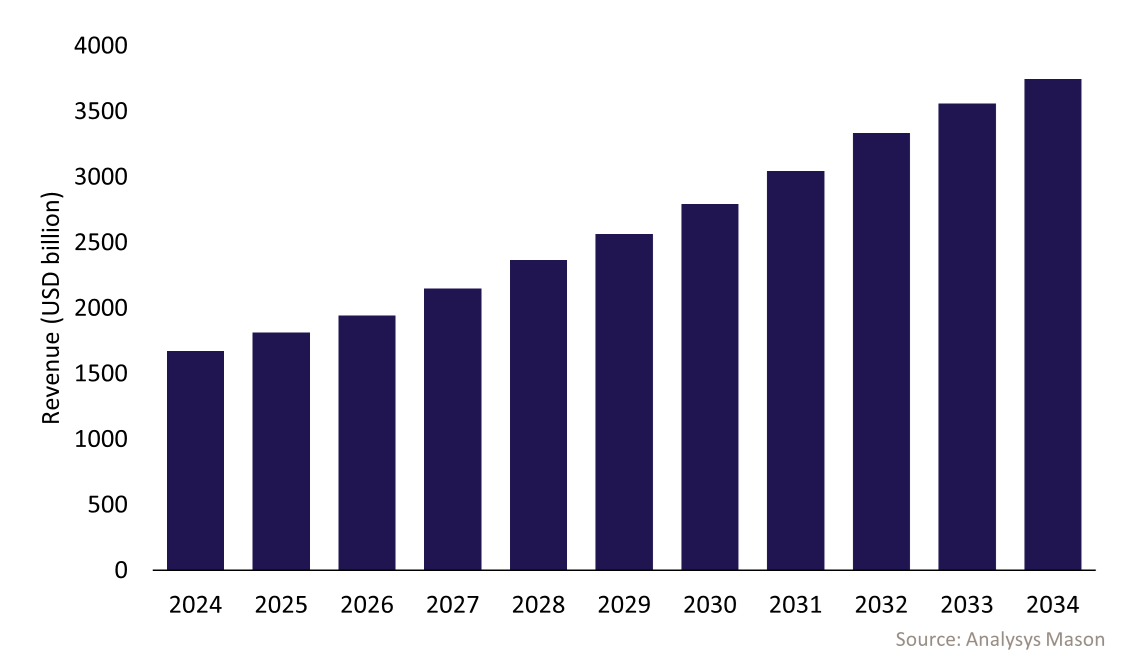

Government demand for EO is very high in defence and intelligence applications, where requirements for persistent monitoring and sovereign control are most acute. The segment represents a USD29 billion opportunity from 2024–2034 (Figure 1).

Figure 1: EO defence and intelligence revenue, worldwide1

Government demand is therefore pushing the market towards satellite-as-a-service (SaaS) models. In this context, vendors will need to deliver secure, end-to-end, analytics-led EO services, rather than just raw imagery, to compete.

Vendors are shifting from imagery supply to software- and analytics-led models

Recent EO activity shows vendors moving away from capital-intensive, imagery-centric business models towards software and analytics.

This shift reflects growing customer demand for decision ready outputs and lower friction access to EO capabilities beyond data procurement, as was traditionally offered by established satellite operators. Deals such as Moody’s acquisition of Cape Analytics illustrate how end users value analytical layers that automate insight generation rather than raw data alone. Similarly, SatSure’s partnership with Dhruva Space signals a move towards integrated service models that merge satellite infrastructure with proprietary analytics that extend beyond EO imagery.

The transition is partly driven by the limitations of capex-heavy EO models. Satellite operators face long satellite development cycles and cost structures that make it difficult to scale with demand. In contrast, SaaS based EO services offer recurring revenues, faster deployment and greater adaptability to sector specific needs. Analytics platforms become central to competitive differentiation as more government and commercial buyers prioritise automated monitoring.

For vendors, this shift requires investment in downstream capabilities: scalable processing pipelines, AI/ML enabled analysis and secure cloud environments that support integration with customer systems. Providers should therefore broaden their offer beyond data supply. If they propose full stack insight delivery, they will be better positioned to capture long term growth.

Recent EO deal activity highlights the importance of sovereign control and secure analytics

2H 2025 activity shows that 72% of satellite manufacturing deals were driven by government customers seeking sovereign control of data. This push is particularly visible across Europe and the USA, where defence organisations are prioritising persistent surveillance from space. The German government’s USD280 million agreement with Planet gives it priority access to high resolution imagery for defence operations amid heightened geopolitical uncertainty. Similarly, the US National Geospatial Intelligence Agency has expanded its reliance on commercial EO providers through Luno B surveillance contracts with BlackSky, Vantor (formerly Maxar) and Ursa, and is operationalising commercial data for national security missions.

Secure analytics is becoming a more explicit part of these requirements. Germany’s agreement with Planet demonstrates this shift: the contract provides government users with priority access to high resolution imagery alongside analytics ready data feeds to support defence and security operations. In parallel, integrated partnerships such as SatSure-Dhruva Space show governments procuring end to end solutions where satellite data and analytical processing are delivered within controlled, domestic frameworks.

These developments create clear expectations for vendors. Providers must ensure secure data flows, compliant cloud environments, resilient supply chains and hybrid delivery models to tap into the government market.

Extending beyond satellites to processing, analytics and operational interfaces under the SaaS model will be essential as sovereign government EO programmes expand. Vendors will need to adapt and provide secure, end-to-end, analytics-led services rather than standalone satellite data.

Analysys Mason’s Earth Observation research programme provides detailed analysis of EO market demand, procurement models and evolving business strategies across defence, public sector and commercial segments. We track developments across the EO value chain, from satellite manufacturing and data access to downstream analytics, platforms and service delivery models. The programme provides clients with market forecasts, competitive assessments and thought leadership to inform their strategic positioning and investment decisions.

1 For more information, see Analysys Mason’s Satellite-based Earth observation: trends and forecasts 2024–2034.

Article (PDF)

DownloadAuthor