The satellite launch bottleneck may soon leave operators stranded

24 April 2026 | Research

Article | PDF (3 pages) | Satellite Manufacturing and Launch | Space

"The satellite launch bottleneck is not a new problem, and operators are soon going to face significant challenges deploying their constellations at all, let alone on time."

Players in the satellite industry have known for years that there is a serious launch problem, referred to as the ’launch bottleneck‘. There is simply not enough available satellite launch capacity to meet demand. Operators will soon become stranded unless they focus on mid-sized platforms, diversify launch provider investment and make allowances for longer timelines for launch vehicle readiness and scheduling.

Satellite operators seem to continuously overestimate launch availability, frequently setting strict deadlines and expectations that they subsequently miss. On 19 April 2026, launch provider Blue Origin’s rocket failed to deploy AST SpaceMobile’s (AST’s) satellite. The satellite was part of AST’s direct-to-device (D2D) constellation, the loss of which represented a setback for AST and for Blue Origin. Despite this setback, AST is aiming to launch 45 satellites in 2026 using Blue Origin’s booster approximately every 30 days. AST’s launch expectations are unrealistically ambitious, a trend that is commonly observed among many satellite operators in the industry.

Satellite launch demand far exceeds supply

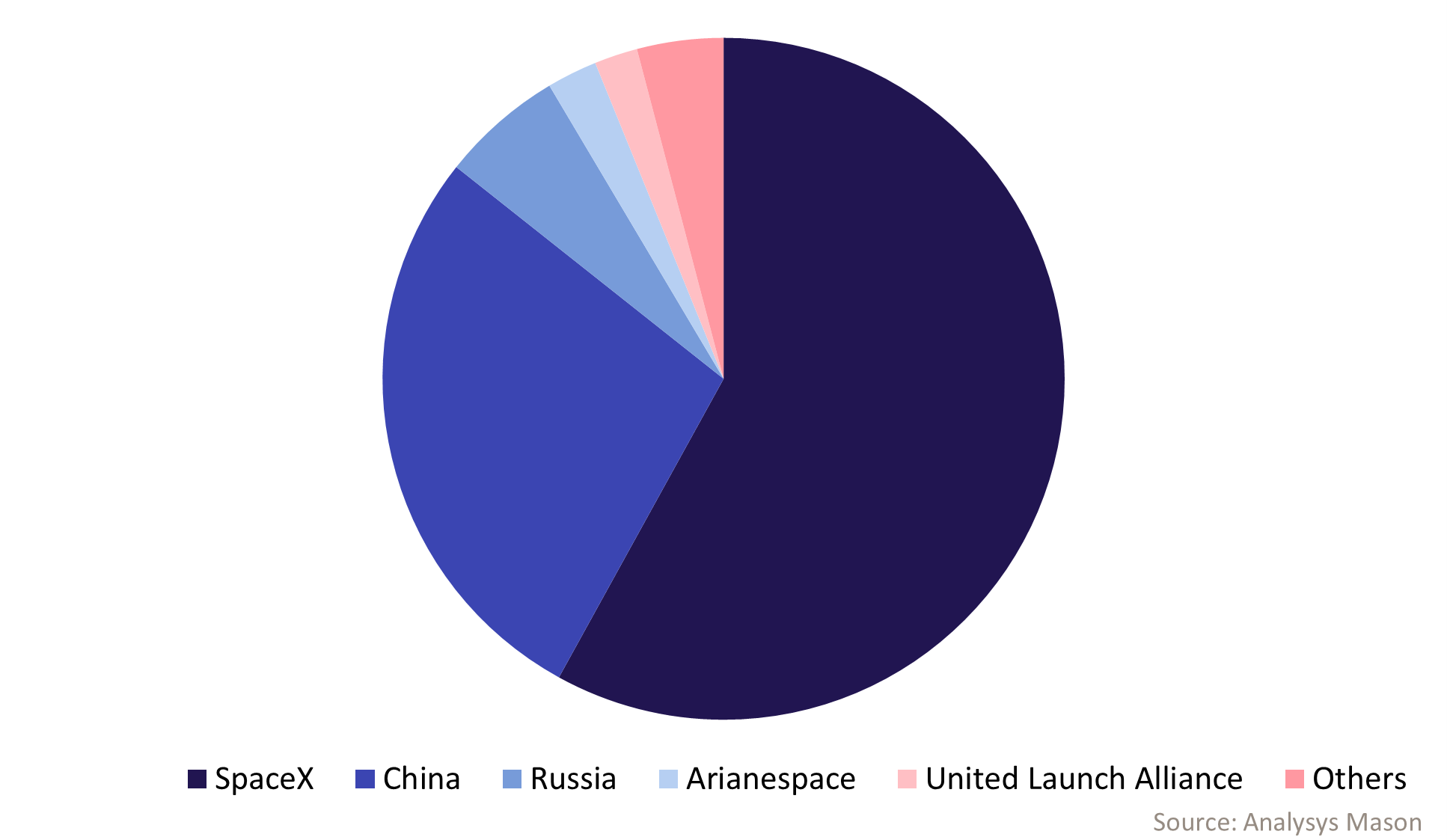

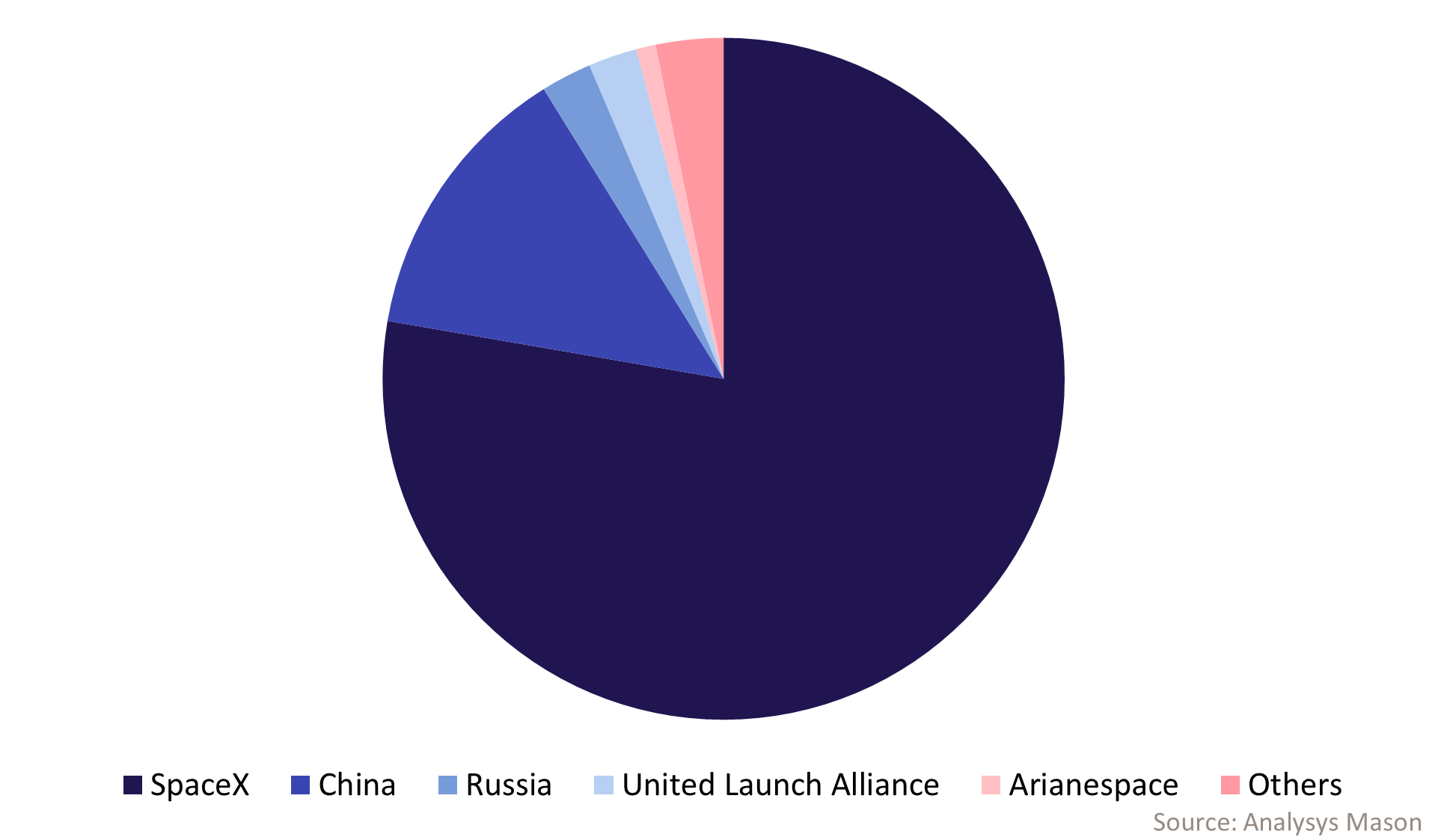

The ‘launch bottleneck’ problem has been obscured from both supply and demand perspectives. Launch cadence has increased worldwide, growing by nearly 50% between 2023 and 2025 – from 223 launches to 330. This growth has been driven and supported by SpaceX, which accounts for 58% of all launches (Figure 1) and 78% of the total mass-to-orbit (or upmass) potential in 2025 (Figure 2).

Established launch service providers (LSPs) such as Arianespace, Blue Origin, MHI, ISRO, Rocket Lab and ULA have all deployed and slowly increased the launch cadence of their new vehicles. Additionally, dozens of new and emerging LSPs (including Isar Aerospace, Latitude, Maia Space, PLD Space and Skyrora) are aiming to bring their vehicles to market in the coming years to add to industry supply.

Figure 1: Satellite launch market share, by number of launches per provider, 2025

Figure 2: Satellite launch market share, by total mass to orbit potential per provider, 2025

SpaceX has nearly doubled its launch cadence in 3 years, launching 170 times in 2025 (compared with 98 times in 2022). The highly anticipated introduction of SpaceX’s Starship rocket is fuelling confidence among satellite operators, many of whom believe that the resulting increase in launch capacity will soon eliminate the launch bottleneck.

From a demand perspective, the market has strongly shifted away from large satellites towards volumes of smaller ones, via constellations. This has given the impression of an easing launch problem because smaller satellites can be launched by a wider pool of LSPs. However, the sheer volume of demand significantly outpaces launch availability. Analysys Mason’s Satellite manufacturing and launch services: trends and forecasts 2024-2034 forecasts that nearly 41 000 satellites will be launched between 2026–2034, and this number does not include the more recently announced orbital data centres from SpaceX (1 million satellites), Starcloud (88 000) and Blue Origin (51 600).

Commercial satellite constellations will soon face competitive pressures and filing problems as deadlines approach

Commercial constellations will soon face a major problem: launch delays impede satellite operator revenue, which risks these players losing market share to other first-movers. For example, AST SpaceMobile wants to launch 45–60 satellites in 2026 and is expecting to be able use Blue Origin’s New Glenn booster every 30 days. Putting aside the fact that Blue Origin only launched twice in 2025, only a few launchers are capable of meeting AST’s demands. The company’s newest Bluebird satellites have a mass close to 6000kg. These high-mass satellites require the largest rockets available in the industry to launch them (many rockets are not powerful enough). The result is that AST’s Bluebird satellites cut the available pool of capable launchers in half (from 104 to 48 available vehicles across 11 LSPs).

However, these 11 LSPs have the largest rockets, so, in theory, AST could realise its goals depending on each LSP’s launch capacity. For example, AST could launch over 1000 satellites this year. However, this theory is based on several variables: 2026 launch performance would need to match that of 2025 (allowing for delays); Bluebird satellites would need to weigh only 5000kg (opening the LSP pool), and AST would have to have access to the entire launch industry. However, 32% of that capacity is provided by Chinese and Russian LSPs, while a further 58% is controlled by SpaceX (the last 10% belongs to the other LSPs that have working, capable rockets, but their launch cadence has not increased significantly in the last 3 years and is not expected to in the near term). Given the strong competition for SpaceX launch capacity across the global market (including from governments and militaries, as well as competition between Starlink and AST, it is difficult to imagine AST SpaceMobile securing capacity access at the necessary scale. If sufficient capacity is unavailable to AST from Chinese and Russian LSPs, or from SpaceX, then AST could launch a conservatively estimated 70 satellites this year, but it would need to capture the as-yet committed global launch capacity in the market.

Meanwhile, Amazon Leo is racing to launch its constellation. Despite contracting multiple LSPs, the company has only launched around 200 satellites, and it must meet a deadline enforced by the FCC to deploy 50% of its constellation (equivalent to 1618 satellites) by July 2026. Applying the same analysis as above, Amazon could theoretically launch 9000 satellites this year across the entire launch market. This figure would fall to 7500 if Chinese and Russian LSPs are excluded, or to only 600 if SpaceX’s rockets are committed to other missions entirely. To date, Amazon has only contracted 13 launches with SpaceX. Even if all other LSPs make moderate improvements in their launch cadences, Amazon would need to launch an additional 26 times with SpaceX to fully deploy its first-generation constellation.

Operators must focus on mid-sized satellites, contract numerous providers and anticipate delays with rocket technology/availability

There are good reasons for the industry phrases “space is hard” and “it’s not rocket science”: developing a working, reliable rocket is technically challenging and expensive, and it requires significant time to increase launch cadence. LSPs will continue working to improve launch market supply, but these developments will take time.

Meanwhile, satellite operators must plan for these constraints rather than basing their strategies on optimistic assumptions such as aggressive launch ramp-ups, or Starship resolving the launch capacity bottleneck. Analysys Mason has seen numerous satellite operators’ business decks that take the above assumptions for granted, using these assumptions to justify strategies that favour larger satellites that can be deployed more quickly and in higher volumes. These strategies will soon leave these operators stranded, waiting for launch.

AST SpaceMobile has diversified its LSPs partners by working with Blue Origin, ISRO and SpaceX, but is too aggressive on its timelines. Amazon has also contracted numerous LSPs and has developed smaller satellites, but it remains too ambitious. Indeed, it is already planning a second-generation constellation of similar size.

To mitigate the launch bottleneck problem, satellite operators should focus on mid-sized platforms, where possible, diversify their investments in launch providers and plan for longer timelines for launch vehicle readiness and scheduling. Otherwise, launch plans risk being undermined by the persistent realities of the launch bottleneck problem.

Analysys Mason’s Satellite manufacturing and launch research programme tracks worldwide activity in the satellite industry, including contracting and launch deployment. Built on 15 years of experience, this research programme includes 10-year forecasts, contract and deals trackers and analysis of technology trends, satellite demand, launch vehicles and satellite constellation development. We support clients in understanding market sizing, technological capabilities, vendor progress and strategy developments as technology, supply and demand trends change.

Download (PDF)

DownloadAuthor

Dallas Kasaboski

Principal Analyst, expert in space infrastructureRelated items

Podcast

D2D: T-Mobile's path to seamless connectivity

Podcast

What's next for GEO satellite operators

Article

Take-private deals are reshaping digital infrastructure, while space companies look to IPOs to support growth