Sovereignty and scale define opportunities in satellite constellation manufacturing

23 April 2026 | Research

Article | PDF | Defence and Sovereign Space| Emerging Space Applications| Satellite Broadband| Satellite Capacity| Satellite D2D| Satellite Manufacturing and Launch| Satellite Mobility| Satellite Networking Technologies| Space Data and AI | Space

"Independent manufacturers that can scale at speed and navigate sovereign markets will harness the potential of constellation demand."

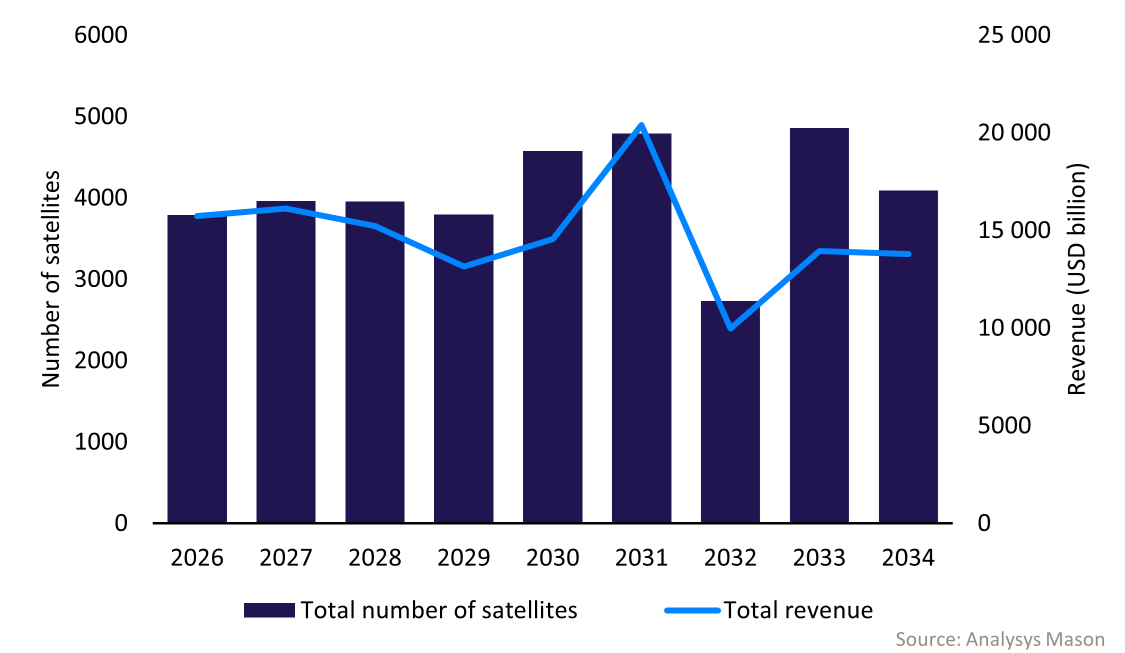

Satellite constellations are poised for growth due to the demand for non-terrestrial networks. Analysys Mason’s Satellite manufacturing and launch services: trends and forecasts projects that a total of 36 528 satellites will be launched as a part of constellations between 2026 and 2034. This represents manufacturing revenue of USD132 billion and, at least in theory, plenty of opportunities for manufacturers (Figure 1).

Despite strong satellite constellation demand, most opportunities remain out of reach for independent manufacturers. Vertically integrated operators, such as SpaceX and Amazon, drive significant market activity, offering satellite platforms, payloads and internal launch services. Residual market activity is much more limited, more fragmented and potentially more restricted by sovereignty concerns. This confines external suppliers to narrowly defined component roles or leaves them excluded altogether.

Figure 1: Total addressable market for manufactured constellation satellites

Announced market activity suggests that the addressable market is overly inflated and inaccessible to the majority of manufacturers. Vendors must position themselves as players that can keep up with the ever-growing constellation demand by adhering to deployment cycles and ambitious constellation scales.

Sovereignty creates protected demand despite constraining market access

In many countries, national policy is increasingly pushing for independent satellite solutions. This trend towards sovereignty provides a growing opportunity for commercial vendors, with governments acting as a demand catalyst. Not only are governments funding constellations in their search for strategic autonomy in communications, navigation and Earth observation, but they are also deliberately shaping domestic supply chains.

Sovereignty comes with a challenge: it can fragment the market, since governments use both soft and hard frameworks to influence the industrial outcome. Soft practices include tenders that are structured to favour domestic bidders and contain evaluation criteria weighted towards local content. Hard practices include export controls, licensing requirements and security restrictions. Even with rising global demand, a manufacturer may still be excluded from entire regions due to jurisdictional boundaries.

Governments are willing to accept these restrictions, despite their limiting effect on access, because they regard space infrastructure as strategic and are reluctant to depend on a single foreign provider. This concern is driving investment in national and regional constellations to develop an indigenous manufacturing capability. For manufacturers, this creates an opportunity in the form of long-term procurement programmes. Policy makers explicitly seek to avoid monopolistic concentration and design competitive tenders to broaden participation in the native ecosystem.

The opportunity favours manufacturers that can scale with the constellation deployment cadence

For component manufacturers, the greatest opportunity lies in targeting large-scale constellations that are still early in their development cycles. This particularly applies to those that have not yet locked in their manufacturing architecture or vertically integrated supply chains.

Lead times represent a decisive differentiator, especially for large-scale production. Providing fast qualification processes and supporting iterative design changes are often more valuable than marginal performance gains. In a market defined by production cadence and replenishment cycles, responsiveness and manufacturing readiness can be as strategically important as technological superiority.

However, manufacturers can only seize this opportunity if they can match the speed of constellation economics. High-volume programmes compress development cycles and demand predictable output. Regardless of technical merit, a supplier will be disregarded if they cannot scale to meet the output requirements, absorb schedule volatility or sustain consistent quality. In this environment, industrial capacity is a competitive asset, not a back-office function.

Analysys Mason’s Satellite Manufacturing and Launch programme tracks and assesses the developments of the satellite constellation market, offering insight, strategy and analysis on the opportunities around satellite constellations. For further information, please contact Dallas Kasaboski.

Download

Article (PDF)Author