The use of OTT video services is becoming nomadic and operators’ strategies need to change

26 May 2020 | Research

Martin Scott | Christopher Ryder

Article | PDF (3 pages) | Video, Gaming and Entertainment

Analysys Mason’s Connected Consumer Survey 2019: TV and video services in Europe and the USA shows that video service stacking was already reaching saturation point in the USA before the COVID-19 outbreak and that the same trend may eventually be seen in Europe. The pandemic has had a number of knock-on effects on the TV and video markets, which may temporarily encourage consumers to stack additional services. However, it has also led to a significant drop in the number of live sports events, which will affect the use of nascent sports streaming services. Non-US pay-TV providers should take a cue from their peers in the USA and consider diversifying their engagement models (and, as a result, their income streams) in order to strengthen their customer relationships and prepare for a longer-term decline in service stacking.

Service stacking is likely to decline after the temporary boost imparted by quarantine measures

The launch of Disney+ in Europe comes at an unusual time because the company has a ‘captive’ audience of consumers that are at home due to the lockdown measures put in place during the COVID-19 pandemic. Initial engagement was strong: by early April 2020 it had more than 50 million paying subscribers. The COVID-19 crisis has no doubt also boosted consumer engagement with other OTT video services, and we expect that the unusual situation will have made consumers more prepared to try free trials of new services. How this will translate into paying customers in the coming months remains to be seen; this will partly depend on how long the pandemic lasts.

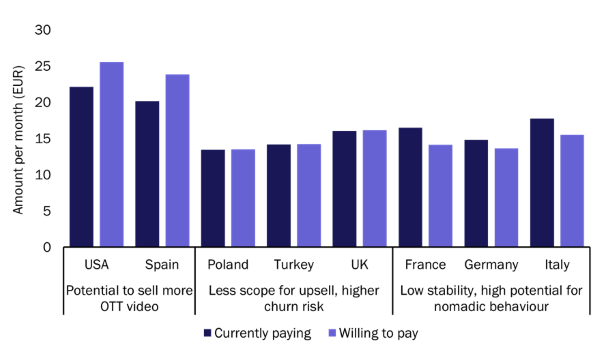

The increased consumer choice provided by the launches of several new OTT video services in 2020 will encourage users to churn from their existing OTT video services. Figure 1 shows that many consumers did not wish to increase their spending on OTT video before the pandemic, and some even planned to reduce their spending, so local video providers should anticipate the coming and going of nomadic subscribers that are trying out new market entrants or are following different hit series and league seasons as they are available. To thrive in this increasingly fluid market, video providers should reconsider the traditional measures against churn in favour of strategies aimed at providing value on both sides, both during and outside of subscriptions.

Figure 1: Current spend on OTT video and the amount that users are willing to pay in the future, by country, Europe and the USA, 2019

Source: Analysys Mason, 2020

Progressive providers are already adapting to this new dynamic and are putting an increased focus on advertising-funded video as an integral part of their offerings. By facilitating downgrades to an ad-supported tier instead of allowing consumers to churn from the service altogether, video providers can retain the relationship with the consumer outside a paid subscription.

The long-term opportunity for revenue growth sits primarily with ad-supported content

The major opportunity for the video industry in the coming years is in advertising; this will account for more than 50% of the projected USD95 billion growth in TV and video revenue between 2019 and 2024. This shift was highlighted at the 2019 MIPCOM conference: AVoD services took centre stage with the announcement of two new major initiatives from Rakuten TV and Lionsgate-backed Tubi. These announcements represent the latest developments in a year of significant activity in the AVoD space; notable other examples include the acquisition of Pluto TV by Viacom, launches by Amazon and Sinclair and announced plans from Comcast/NBCUniversal and WarnerMedia. There also appears to be a demand-side justification for introducing ad-subsidised/funded tiers: 70% of US player Hulu’s active user base subscribed to the cheaper ad-supported tier rather than the more-expensive ad-free version in May 2019.1

In order to embrace opportunities in advertising, video providers should consider customer journeys where subscribers move freely across their various business models and should prioritise long-term relationships over short-term profits. By combining advertising, transactional, subscription-based and aggregator business models, video providers can address the entire spectrum of user needs from offering a single piece of content to becoming the go-to platform for content and recommendations. When implemented successfully, this will enable providers to add value for both themselves and their customers in an increasingly nomadic market.

Operators’ response to a dynamic market must be a dynamic business model

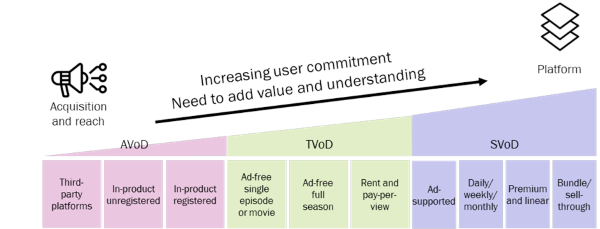

With such a sliding scale for user commitment, free or advertising-funded models may be able to serve either as the entry point to customer journeys or as the point to which existing customers retrench as their wants and needs change. Usage data gained through these models can then be used to build the upgrade path back along the ladder of increasing engagement and commitment in a hybrid business model. Increased user commitment along the ladder needs to be underpinned by a matching increase in value and user understanding, as illustrated in Figure 2 below. Successful services will be based on users’ needs and intents, rather than the underlying business models, which should be adapted to fit the offering, not the other way around.

Figure 2: Hybrid business model for video

Source: Analysys Mason, 2020

Allowing users to move freely up and, importantly, down the ladder of business models in a single offering based on their changing needs and wishes can remove the friction that could make customers churn out of the relationship and significantly lengthen the journey to them becoming paying customers again. Creating products and experiences that fit into users’ lives on their terms is the key to success in the years to come, and the tools to do so are found in the inspired use of data and the re-thinking of existing business models.

1 Tubefilter (2019), 70% Of Hulu’s 28 Million Subscribers Are On Its Ad-Supported Tier – And Hulu’s Innovating Ads To Keep Them There. Available at: https://www.tubefilter.com/2019/05/29/hulu-how-many-subscribers-ad-supported-tier/.

Download

Article (PDF)Authors

Martin Scott

Research Director

Christopher Ryder

Principal, expert in transaction servicesRelated items

Forecast report

Czech Republic: pay TV and streaming video forecast 2023–2029

Article

Telecoms operators will become even more important to streaming providers as service stacking stalls

Forecast report

Poland: pay TV and streaming video forecast 2024–2029