Operators are relying on IT services for growth, but their position looks vulnerable

30 June 2026 | Research

Article | PDF | SME Services| Enterprise Services | IT Services

"Operators should respond quickly to changing market, economic and technological conditions to maximise their chances of achieving revenue growth from IT services."

Analysys Mason forecasts strong growth in telecoms operators’ revenue from IT services. However, achieving this growth is not a given for individual operators. Failure to maintain pace with developments in IT markets could lead to operators losing business to competitors. Operators are also vulnerable to changing market conditions, including disruption from low-cost service providers and step changes in technological developments.

Operators must continue to invest in the necessary capabilities and partnerships to expand their B2B portfolios. They should also be ready to respond quickly to changing market conditions, for example by making small, early-stage investments in emerging technologies such as AI agents and quantum computing.

Analysys Mason’s baseline B2B forecasts anticipate significant growth in operator revenue from IT services

Analysys Mason projects that operator revenue from IT services for business customers will grow at a CAGR of 7.1% for large businesses and 8.2% for SMEs (in nominal terms) in the period to 2030.

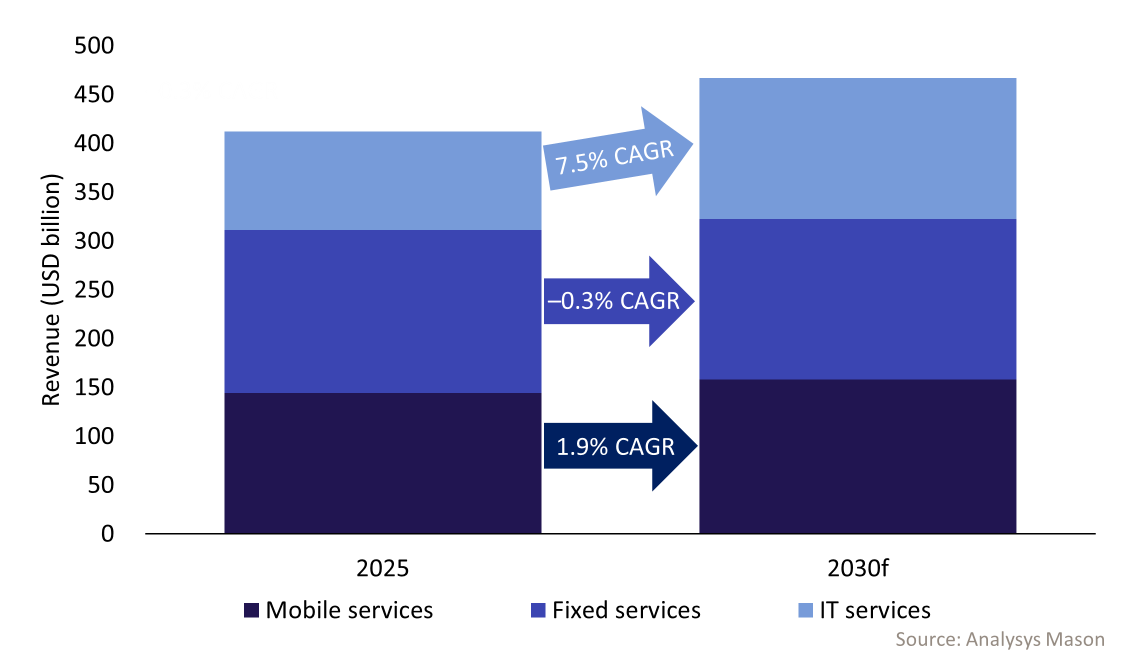

Growth in B2B revenue from connectivity services will be more muted. We expect mobile service revenue to rise at roughly the rate of inflation, driven mainly by an increase in mobile IoT connectivity revenue. Mobile private networks could provide a further uplift for some operators, as could network prioritisation for business-critical services. However, neither of these solutions are expected to make a significant impact on total mobile B2B revenue by 2030. Fixed service revenue is projected to decline in most regions. This leaves most operators reliant on IT services to drive revenue growth (Figure 1).

Figure 1: Telecoms operators' retail revenue from businesses by service type, worldwide

There are good reasons to be optimistic about operators maintaining or increasing their share in IT markets

Analysys Mason expects most operators to maintain or improve their position in the B2B IT services market relative to competitors such as systems integrators (SIs), managed service providers (MSPs) and IT specialists. We consider this to be the most plausible outcome, considering the following factors:

- business demand for integrated connectivity and IT services. Businesses also want to reduce the number of different suppliers used

- operator supply of an increasing range of IT services within their portfolios, often supported by professional services and systems integration capabilities.

In some regions, we expect a slight increase in operator market share for cyber security. More than 10 operators have made acquisitions since the start of 2024 to support their security propositions. Some have established dedicated cyber-security practices (for example, Bell Cyber launched in September 2025). Growth in SASE and other integrated connectivity and security services offers another opportunity for operators, and many security vendors view telecoms operators as a key route to market.

However, failure by operators to provide adequate professional and managed services (either directly or via partners), or to maintain pace with developments in IT markets, could lead to a loss of business to competitors. This has already occurred in some countries (including the USA and Australia) where operators have stepped back from offering certain IT services.

Operators are vulnerable to changing market, economic and technological conditions

Disruptive pricing moves from challenger operators could cause connectivity revenue to grow more slowly (or to decline faster). Our forecasts factor in existing players such as Digi and Iliad in Europe, but there is potential for these players to expand further or for satellite operators to compete aggressively using excess capacity. This would have a major impact on consumer services, but lower consumer prices tend to lead to pressure on prices for business-grade connectivity. Some low-cost service providers also target SME customers with connectivity and IT services bundles.

Economic conditions may also present challenges for operators. We expect the number of employees and businesses to remain stable at a global level between 2025 and 2030. However, in some countries (especially in Europe and some parts of APAC), the working-age population will decline, reducing demand for business services. Geopolitical events could also disrupt economic conditions, leading to businesses postponing IT investments. This could be exacerbated by problems with the supply of key components.

Analysys Mason’s baseline forecasts account for our view of likely technological developments, including adoption of AI and software advancements in areas such as network management and cyber security. However, there is potential for more extreme scenarios to cause significant variation from these. For example:

- More rapid advances in AI’s ability to improve productivity, which could lead to a widespread reduction in demand for white-collar workers, who have typically been the highest users of mobile and IT services. This could have a significant impact on operators’ revenue from user-driven IT services such as cloud voice and collaboration tools.

- An unexpected step change in traffic volumes caused either by massive adoption of agentic AI or data-intensive services such as AI video monitoring or XR calling. This could lead to increased demand for high-capacity data connectivity, and potentially increased revenue from associated IT services.

- Rapid advances in quantum computing, leading to ‘Q-Day’ arriving sooner than expected. This would lead to accelerated demand for quantum-safe networking solutions, favouring operators that have already established commercial services.

Operators should continue to invest in new capabilities and be ready to respond quickly to disruptive trends

IT services will account for most B2B revenue growth for most operators. However, only operators that invest in the necessary capabilities and partnerships to expand their portfolios will benefit. Operators need to be willing to invest in services that have lower EBITDA margins than connectivity but can still benefit their business financially.

Operators should also be ready to respond quickly to changing market, economic and technological conditions. This might include willingness to counter aggressive pricing strategies from competitors or exploring investments in sovereign infrastructure and services. From a technological perspective, investing in start-ups and conducting early trials with emerging technologies such as AI agents and quantum computing can help position operators to take advantage of new commercial opportunities. Returns are uncertain, but it is likely that at least some will succeed, and small, early-stage investments will help operators to scale quickly when demand emerges.

Analysys Mason’s business and IT services forecasts include revenue and volume projections by size of business for more than 50 individual countries worldwide. Our business services research programmes support operators to develop propositions that will make the most of opportunities to drive growth in B2B revenue and profitability. Please contact Catherine Hammond to learn more or to discuss any of the ideas highlighted in this article.

Download

Article (PDF)Author